- StocksGeniusMastery

- Posts

- 💥 Broadcom vs. AMD: Which AI Chip Stock Has More Upside?

💥 Broadcom vs. AMD: Which AI Chip Stock Has More Upside?

Strong growth, rising analyst optimism, and a valuation gap are setting up a decisive investor showdown.

Bensheares Parker

March 12, 2026

In partnership with

Hi Fellow Investors,

Broadcom (NASDAQ: AVGO) and Advanced Micro Devices (NASDAQ: AMD) are both benefiting from surging demand for AI chips from hyperscalers and major model developers.

The key debate now is not whether these companies can grow, but which stock offers the stronger mix of momentum, scale, and valuation.

This comparison points to two high-quality AI contenders, with one appearing more attractively priced at current levels.

Key Points:

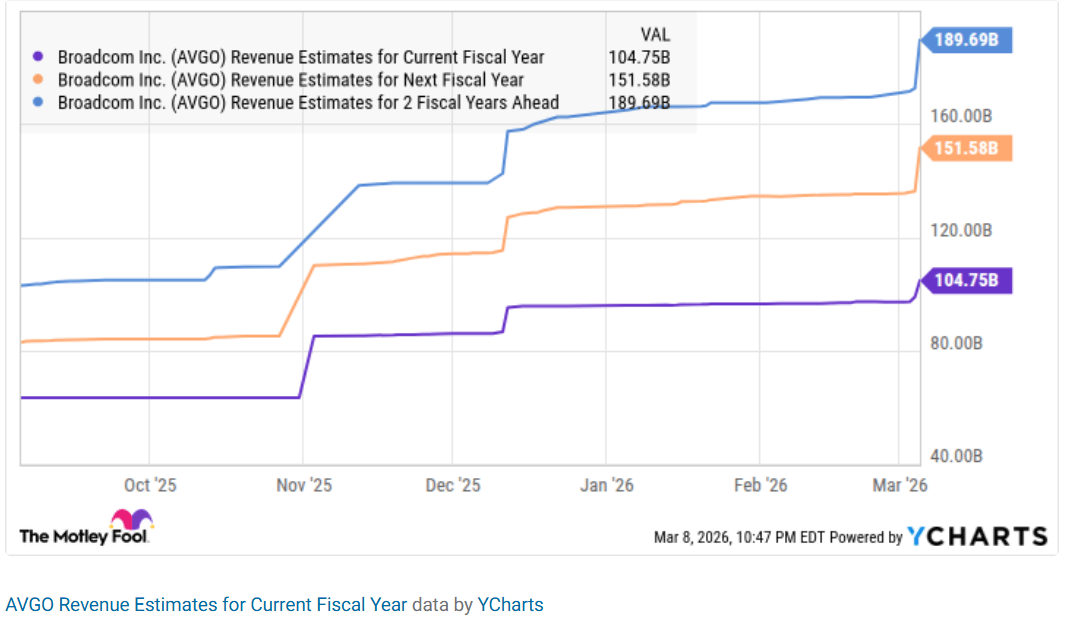

Broadcom’s AI business is accelerating rapidly as custom AI chip demand gains traction across some of the world’s largest technology customers.

AMD’s data center expansion and GPU adoption are improving meaningfully, giving the company a stronger long-term foothold in AI infrastructure.

Valuation may be the deciding factor, as AMD trades at a far lower sales multiple even though both companies still have powerful growth catalysts.

TODAY’S SPONSOR

Attio is the AI CRM for modern teams.

Connect your email and calendar, and Attio instantly builds your CRM. Every contact, every company, every conversation, all organized in one place.

Then Ask Attio anything:

Prep for meetings in seconds with full context from across your business

Know what’s happening across your entire pipeline instantly

Spot deals going sideways before they do

No more digging and no more data entry. Just answers.

Broadcom’s Custom AI Engine Is Firing on All Cylinders

Broadcom (NASDAQ: AVGO) is emerging as one of the biggest winners in custom AI processors, where hyperscalers are increasingly looking for alternatives to general-purpose accelerators.

Its dominant position in ASICs gives it direct exposure to a fast-growing part of the AI server market.

First-quarter fiscal 2026 AI revenue more than doubled year over year, showing that demand is no longer theoretical.

That momentum is being supported by an elite customer roster that includes major cloud and AI platform builders.

Management’s confidence in scaling to dramatically higher AI revenue by 2027 signals that this growth story may still be in its early innings.

Strengths

Broadcom has a powerful leadership position in custom AI chips, giving it exposure to one of the most attractive niches in semiconductor infrastructure.

Its customer base includes top-tier hyperscalers and AI leaders, which strengthens revenue visibility and reinforces execution credibility.

AI revenue growth is already surging, and management’s longer-term targets suggest the company could unlock another major leg of expansion.

Weaknesses

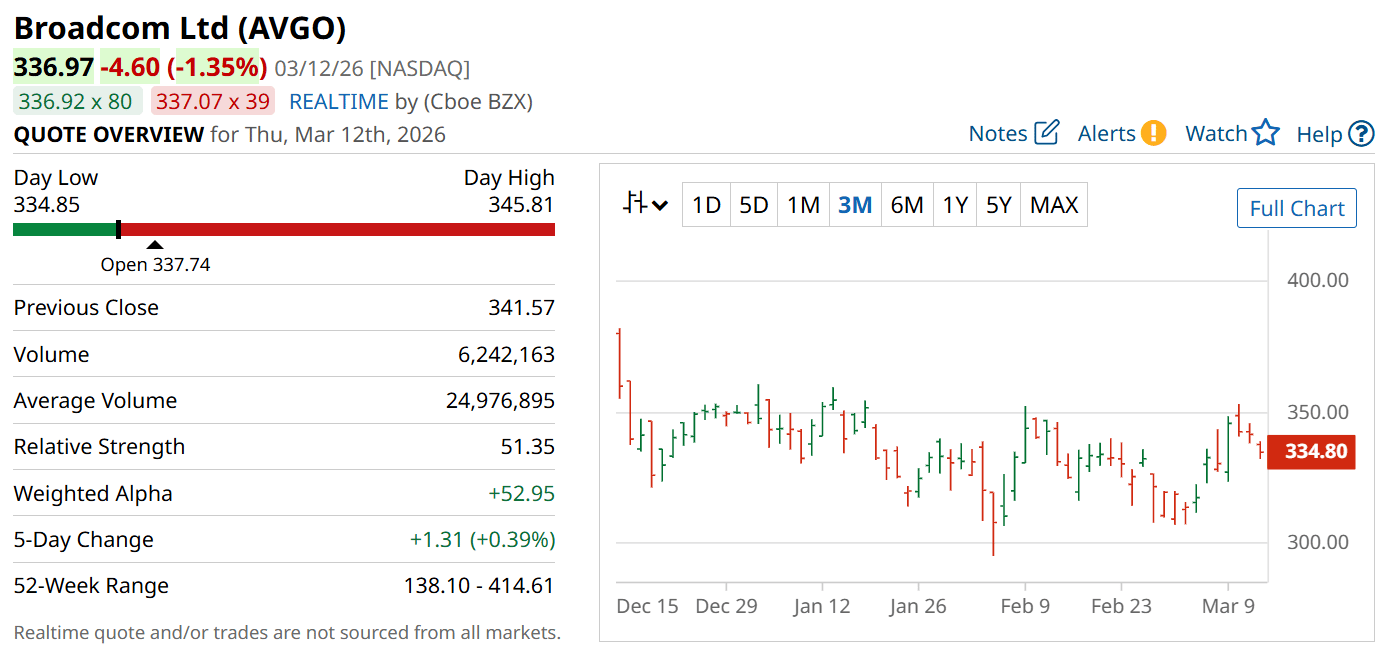

Broadcom’s premium valuation leaves less room for disappointment if growth slows or customer deployments take longer than expected.

A large portion of investor enthusiasm now depends on continued success in AI, raising the pressure on flawless execution.

The stock’s massive run could make near-term upside harder to achieve without another round of outsized results.

Potential

Broadcom could become the defining custom AI infrastructure winner as ASIC adoption rises across the data center market.

If management comes close to its long-range AI revenue ambitions, today’s valuation could look much more reasonable in hindsight.

Continued customer scaling from companies like Meta, OpenAI, and Anthropic could keep estimates moving higher.

AMD’s AI Comeback Is Becoming Harder to Ignore

Advanced Micro Devices (NASDAQ: AMD) continues to trail Nvidia in AI GPUs, but its position is improving as large-scale deployments begin to expand.

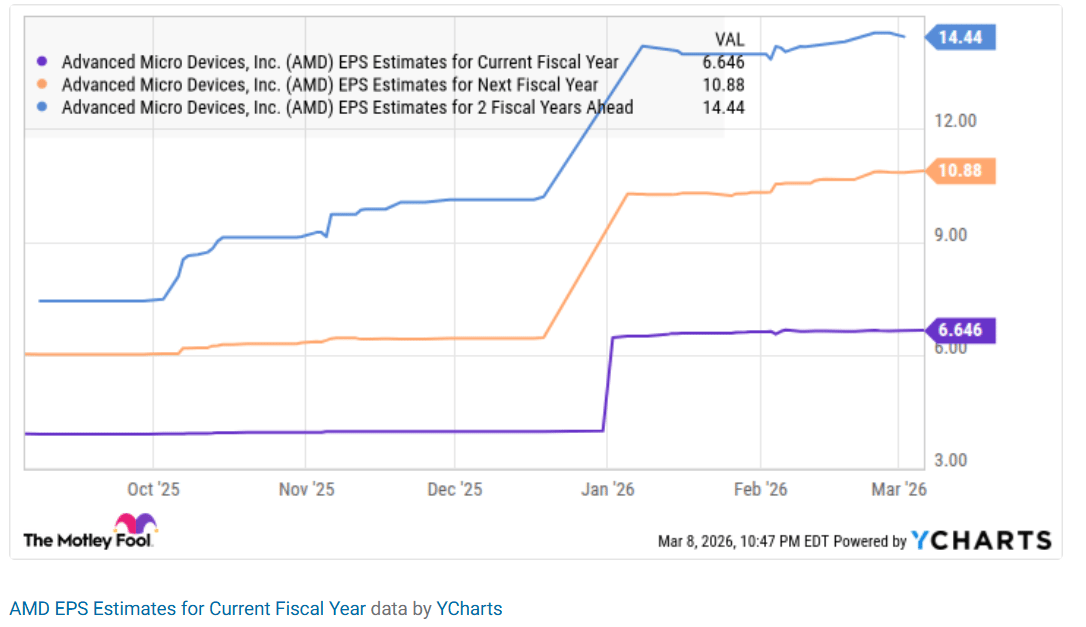

Data center revenue growth shows the company is making real progress in one of the most important battlegrounds in semiconductors.

Its Instinct GPUs are gaining traction, and multibillion-dollar customer deals suggest AMD is no longer just an outside challenger.

The business also has multiple supporting catalysts, including AI PCs and stronger server CPU relevance.

With analysts forecasting powerful earnings growth, AMD appears to have both improving fundamentals and a more forgiving valuation profile.

Strengths

AMD is building real momentum in data center AI, with GPU adoption helping push revenue growth at an encouraging pace.

The company has secured meaningful customer commitments that could materially expand its compute footprint over time.

Its business is supported by several growth engines beyond AI GPUs, including server CPUs and AI-enabled personal computing.

Weaknesses

AMD still remains behind Nvidia in the AI accelerator race, which limits its influence in the most dominant segment of the market.

Execution risk remains elevated because future gains depend on turning design wins and contracts into sustained large-scale deployments.

Margins and competitive positioning are not yet as strong as those of the very top players in AI chips.

Potential

AMD could unlock substantial upside if it achieves a double-digit share of the data center GPU market over the next several years.

Major customer agreements with large AI and cloud players could transform market perception and revenue power.

Its lower valuation gives the stock more room to rerate higher if earnings growth continues to surprise positively.

TODAY’S SPONSOR

270 Million Stems Sold And Counting

With 270 million stems sold and $90M+ in recent revenue, The Bouqs Co. has proven its market dominance. Now, the floral ecommerce leader is launching 70+ retail studios to capture more high-margin event and same-day delivery markets. Become a shareholder in The Bouqs Co.

Invest in The Bouqs Co.

This is a paid advertisement for The Bouq’s Regulation CF offering. Please read the offering circular at https://invest.bouqs.com/

Conclusion

Broadcom looks like the more dominant AI infrastructure play, especially for investors seeking scale, customer depth, and custom-chip leadership.

AMD, however, stands out as the more attractively valued opportunity, with strong growth catalysts that could reward investors if execution stays on track.

For investors choosing between the two today, AMD appears to offer the slightly better blend of upside potential and valuation support.

Final Thought

Broadcom may have the stronger AI grip today, but AMD could be the stock that delivers the bigger surprise if market share gains continue to build.

When two quality semiconductor winners are both riding the same megatrend, valuation often becomes the edge that matters most.

Can I ask a small favor from you if you find the content useful to you? Spread the wealth by sharing my FREE Newsletter with fellow stock investors and friends and help to check out my sponsor advertisement and that will keep me writing more stocks newsletters!

Of course, you should always do your own research and due diligence before investing in any stock. You should also diversify your portfolio and balance your risk and reward too!

~ Final Thought: "Fortune Favors the Bold: Embrace Opportunity Property, Execute Strategy, and Reap the Rewards of Investing Wisely.”🌱

What's Your Take on Our Newsletter? 🌟We're eager to hear your thoughts so we can make our newsletter even more amazing for you! |

Disclaimer: The content provided on this blog is for educational and informational purposes only and is not intended as financial, investment, tax, or legal advice. Investing in the stock market involves risks, including the loss of principal. The views, thoughts, and opinions expressed in this blog are solely those of the author and do not reflect the views of any company, organization, or other group. Readers are encouraged to perform their own research and due diligence before making any financial decisions and actions based on the content. Neither the author nor the publisher is liable for any losses or damages arising from the use of the advice or information contained herein.

Reply