- StocksGeniusMastery

- Posts

- 💥 Micron’s AI Supercycle: How High Could MU Go by Year-End 2026?

💥 Micron’s AI Supercycle: How High Could MU Go by Year-End 2026?

With forward P/E near 12, the discount to Nvidia and AMD is impossible to ignore.

Bensheares Parker

February 16, 2026

In partnership with

Hi Fellow Investors,

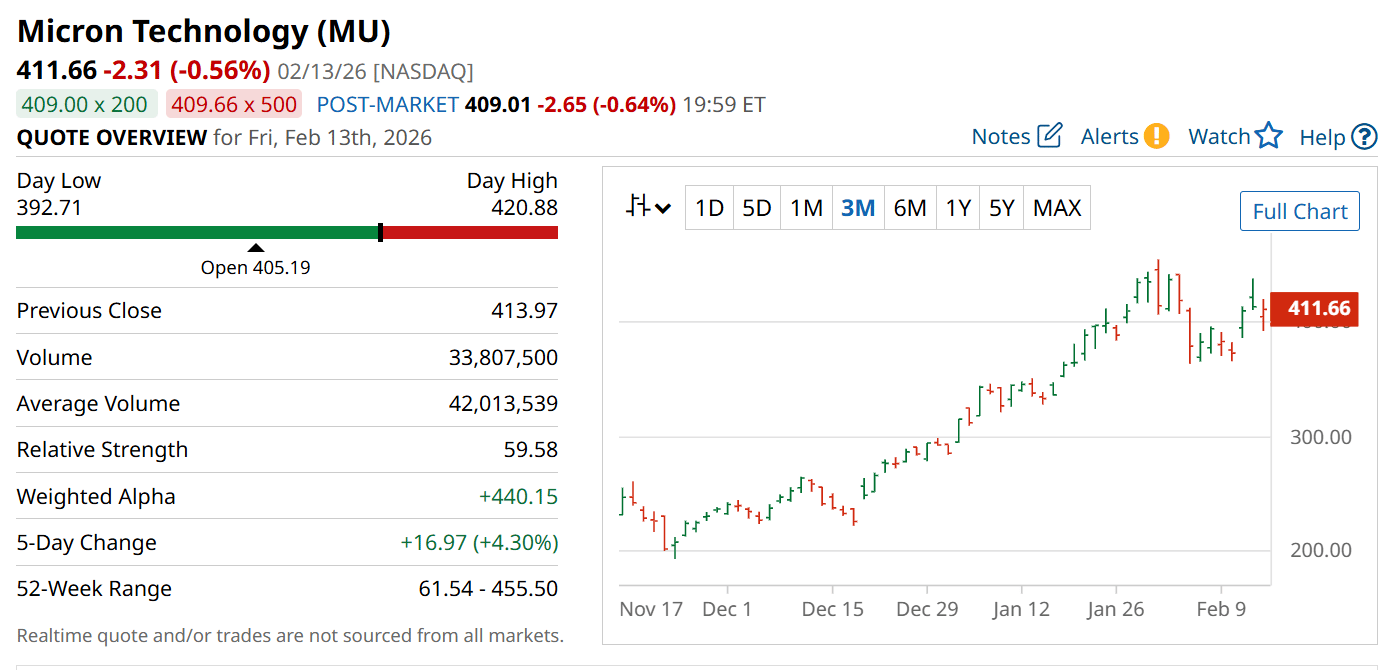

Micron Technology (NASDAQ: MU) is emerging as one of the most compelling AI infrastructure plays of 2026.

Hyperscaler capital spending is expanding beyond GPUs and increasingly targeting memory and storage.

Despite explosive growth forecasts, Micron still trades at a steep valuation discount to AI chip peers.

Key Points:

Hyperscaler capex is shifting toward high-bandwidth memory, creating a structural demand tailwind.

Micron’s revenue is projected to grow roughly 81% in 2026, with earnings expected to triple.

At just 12 times forward earnings, Micron trades far below other leading AI semiconductor stocks.

TODAY’S SPONSOR

AI in HR? It’s happening now.

Deel's free 2026 trends report cuts through all the hype and lays out what HR teams can really expect in 2026. You’ll learn about the shifts happening now, the skill gaps you can't ignore, and resilience strategies that aren't just buzzwords. Plus you’ll get a practical toolkit that helps you implement it all without another costly and time-consuming transformation project.

For years, Micron was viewed as a cyclical memory supplier tied to consumer upgrade cycles.

The AI boom is fundamentally altering that narrative.

Cloud giants and AI developers are building infrastructure for advanced models, robotics, autonomous vehicles, and intelligent agents.

While GPUs power training and inference, memory and storage have become critical bottlenecks.

Micron’s high-bandwidth memory solutions sit directly at the center of that constraint.

As AI workloads scale, memory intensity per system continues to rise dramatically.

Sold-Out Supply Signals a Powerful Upcycle

Management has indicated that existing inventory is already fully committed.

That visibility provides rare clarity in a historically volatile memory industry.

Wall Street now expects revenue to reach roughly $76 billion this fiscal year, implying 81% growth over trailing sales.

Earnings per share are forecast to nearly triple as operating leverage expands.

Micron is simultaneously investing in additional manufacturing capacity to meet surging demand.

These supply-demand dynamics resemble the early stages of a semiconductor supercycle.

Valuation Gap Creates Asymmetric Upside

Despite this acceleration, Micron trades at roughly 12 times forward earnings.

By comparison, Nvidia trades near 25 times forward earnings, AMD near 32, Broadcom near 34, and Taiwan Semiconductor near 27.

Even the Nasdaq-100 index carries a forward multiple around 25.

If Micron merely re-rated closer to peer averages, shares could approach $800 or higher.

A more conservative scenario points toward $650 as a realistic year-end 2026 target.

The discount suggests investors still view Micron as cyclical rather than structurally transformed.

Strengths

High-bandwidth memory leadership positions Micron at the core of AI infrastructure expansion.

Revenue and earnings growth forecasts for 2026 are among the strongest in the semiconductor sector.

A forward P/E near 12 offers significant multiple expansion potential relative to AI peers.

Weaknesses

Memory remains inherently cyclical, exposing margins to supply imbalances.

Rapid capacity expansion could pressure pricing if demand moderates.

Investor sentiment may shift quickly if hyperscaler spending slows.

Potential

AI-driven memory intensity could structurally extend the current upcycle beyond historical patterns.

Valuation re-rating toward peer multiples could push shares into the $650–$800 range.

Sustained hyperscaler capex may transform Micron into a long-term compounder rather than a boom-bust play.

TODAY’S SPONSOR

Snippets that scale your voice

Save and insert standard intros, calendar links, and bios by voice so recurring emails and updates take seconds. Wispr Flow keeps your tone and speeds execution. Try Wispr Flow for founders.

Conclusion

Micron sits at the intersection of explosive AI demand and a deeply discounted valuation.

If revenue and earnings projections materialize, meaningful upside appears achievable in 2026.

A move toward $650 or higher by year-end reflects both growth acceleration and multiple expansion potential.

Final Thought

In past cycles, memory stocks peaked quickly and fell just as fast.

Could AI demand finally break that pattern and redefine Micron’s long-term trajectory?

Can I ask a small favor from you if you find the content useful to you? Spread the wealth by sharing my FREE Newsletter with fellow stock investors and friends and help to check out my sponsor advertisement and that will keep me writing more stocks newsletters!

Of course, you should always do your own research and due diligence before investing in any stock. You should also diversify your portfolio and balance your risk and reward too!

~ Final Thought: "Fortune Favors the Bold: Embrace Opportunity Property, Execute Strategy, and Reap the Rewards of Investing Wisely.”🌱

What's Your Take on Our Newsletter? 🌟We're eager to hear your thoughts so we can make our newsletter even more amazing for you! |

Disclaimer: The content provided on this blog is for educational and informational purposes only and is not intended as financial, investment, tax, or legal advice. Investing in the stock market involves risks, including the loss of principal. The views, thoughts, and opinions expressed in this blog are solely those of the author and do not reflect the views of any company, organization, or other group. Readers are encouraged to perform their own research and due diligence before making any financial decisions and actions based on the content. Neither the author nor the publisher is liable for any losses or damages arising from the use of the advice or information contained herein.

Reply