- StocksGeniusMastery

- Posts

- 💥Nvidia vs. Alphabet: Which AI Titan Is the Smarter Buy for 2026?

💥Nvidia vs. Alphabet: Which AI Titan Is the Smarter Buy for 2026?

Investors face a high-stakes choice between breakout momentum and diversified cash-flow strength.

Bensheares Parker

April 04, 2026

In partnership with

Hi Fellow Investors,

Artificial intelligence has become a major growth engine for Nvidia (NASDAQ: NVDA) and Alphabet (NASDAQ: GOOGL).

Both companies are helping define the next era of computing, but one appears better positioned for investors seeking the strongest mix of upside, resilience, and long-term predictability.

Key Points:

Nvidia continues to deliver extraordinary AI-driven growth, but its premium valuation and hardware cyclicality raise the stakes.

Alphabet combines strong AI momentum with a diversified business model, rising cloud profitability, and massive free cash flow.

While both remain elite long-term businesses, Alphabet looks like the better buy right now based on durability and risk-adjusted return potential.

TODAY’S SPONSOR

Market Volatility Exposes Weak Delegation

When markets get shaky, advisors don’t just manage portfolios. They manage fear, questions, follow-up and a flood of client communication.

That’s where weak delegation gets expensive.

If meeting prep, paperwork, CRM updates and account admin still run through you, response times slip and the client experience takes the hit.

BELAY created the free Financial Advisor’s Delegation Guide to help you identify what to hand off, what to keep and how to stay client-facing without losing control.

Inside, you’ll learn how to reduce bottlenecks, protect responsiveness and free up more time for the work only you should be doing.

Nvidia’s AI Machine Is Still Firing on All Cylinders

Nvidia’s recent results showed that the company remains the most powerful picks-and-shovels play in the AI boom.

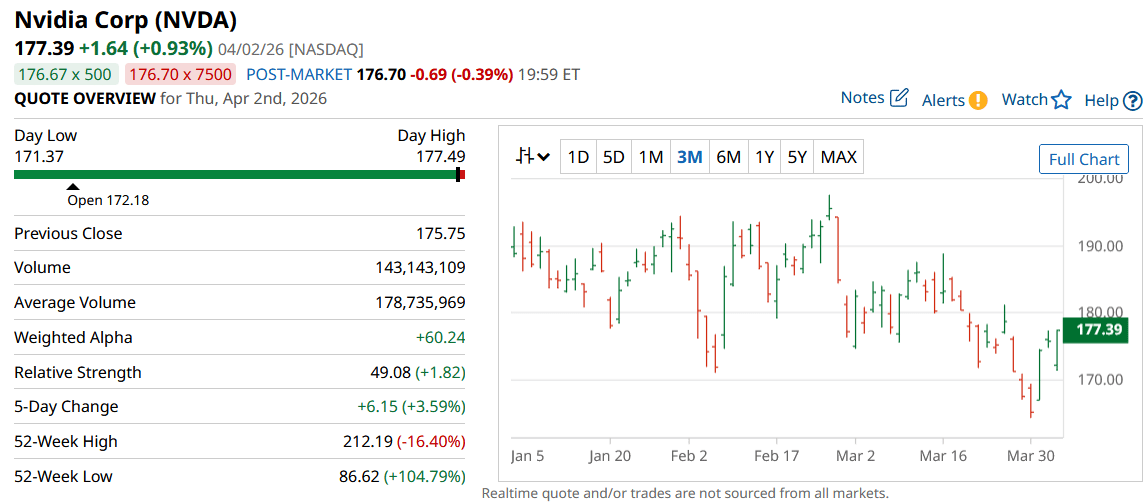

Fiscal fourth-quarter revenue surged 73% year over year to $68.1 billion, with data center revenue contributing a staggering $62.3 billion.

That performance confirms that hyperscalers and enterprise customers are still spending aggressively on AI infrastructure.

Demand remains so strong that even older product lines continue to sell out, underscoring just how tight the supply environment still is.

Few companies in the market can match Nvidia’s current momentum, pricing power, or strategic relevance in the AI buildout.

Nvidia’s challenge is not execution, but expectations.

The company’s business is still heavily tied to capital spending cycles from a concentrated group of giant cloud customers.

That means any slowdown in AI infrastructure budgets, shift toward in-house custom chips, or easing in supply-demand imbalances could pressure both growth and margins.

A stock trading around 36 times earnings leaves limited room for operational missteps or a cyclical reset in hardware demand.

Nvidia may continue outperforming in the near term, but the long-term path likely comes with more volatility than many investors expect.

Strengths

Nvidia remains the clearest hardware backbone of the AI revolution, and its revenue acceleration proves demand is still exceptionally strong.

Its dominance in AI GPUs gives it rare pricing power and strategic leverage as cloud giants race to expand compute capacity.

The company’s scale, brand, and technology leadership make it one of the most important enablers of next-generation computing.

Weaknesses

Nvidia’s growth is deeply tied to customer capital expenditure cycles, which can turn quickly when infrastructure spending normalizes.

The stock’s premium valuation creates little margin for error if demand cools or competitive pressure increases.

Heavy dependence on AI chip demand makes the business more cyclical than many software-centric megacap peers.

Potential

Nvidia could keep compounding at an elite rate if AI adoption remains early and global compute demand continues exploding.

New chip cycles, continued cloud expansion, and enterprise AI deployment could extend its leadership far longer than skeptics expect.

If management sustains this pace of innovation, Nvidia could remain one of the market’s most powerful secular winners for years.

Alphabet’s AI Story Looks Slower, but Far More Durable

Alphabet’s growth may not look as dramatic as Nvidia’s, but the company’s AI opportunity is broad, diversified, and increasingly profitable.

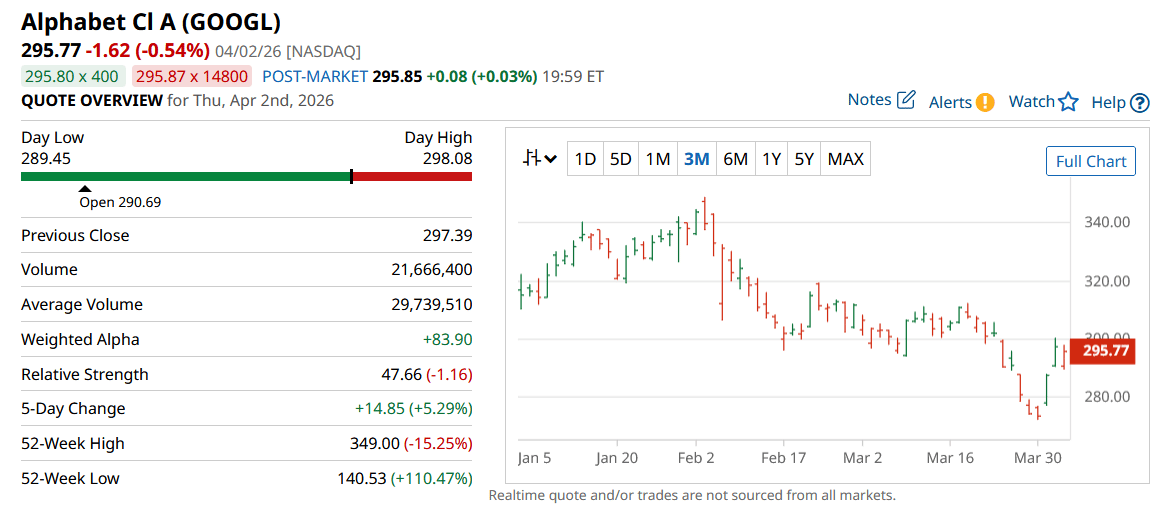

Fourth-quarter revenue climbed 18% year over year to $113.8 billion, supported by strength in digital advertising and cloud computing.

Its ad business still generates the bulk of revenue, giving the company a powerful cash engine that funds aggressive AI investment.

At the same time, Google Cloud is emerging as a major second pillar of growth and profitability.

That combination gives Alphabet a rare ability to invest heavily in AI without relying on a single product category or hardware cycle.

Google Cloud Is Becoming the Real Power Move for Alphabet Investors

Google Cloud revenue jumped 48% year over year to $17.7 billion, and operating margin expanded sharply to 30.1%.

That margin improvement suggests Alphabet is not just growing cloud revenue fast, but scaling the business in a highly efficient way.

Management also highlighted larger customer commitments, including a surge in billion-dollar deals that points to deepening enterprise demand.

A cloud backlog of $240 billion adds another layer of confidence that this momentum is not a short-lived spike.

For investors, that creates a compelling setup where a mature ad giant is simultaneously building a fast-growing, high-margin enterprise AI business.

Why Alphabet Looks Like the Better Buy Right Now

The case for Alphabet comes down to durability, diversification, and downside protection.

Unlike Nvidia, Alphabet is not dependent on a single hardware spending wave to justify its valuation.

Its search, YouTube, and broader advertising ecosystem generate massive user engagement and $73.3 billion in annual free cash flow, giving the company more flexibility if one growth engine slows.

Even with elevated capital spending plans tied to AI and cloud infrastructure, Alphabet appears better positioned to absorb those investments and turn them into long-term shareholder value.

At roughly 27 times earnings, the stock also offers a more forgiving valuation than Nvidia while still providing meaningful exposure to the AI era.

Strengths

Alphabet pairs AI upside with one of the world’s most durable digital ecosystems, anchored by Search, YouTube, and Cloud.

Google Cloud is growing rapidly and becoming far more profitable, giving investors a powerful second engine beyond advertising.

Massive free cash flow gives management the firepower to invest aggressively in AI without weakening the broader business.

Weaknesses

Alphabet’s growth rate still trails Nvidia’s, which may make the stock look less exciting in momentum-driven markets.

Heavy capital spending on AI infrastructure raises pressure on management to prove attractive returns on investment.

Regulatory scrutiny and competitive pressure in search and advertising remain ongoing risks that investors cannot ignore.

Potential

Alphabet could emerge as one of the biggest AI winners if it successfully monetizes AI across search, cloud, productivity, and consumer platforms.

The company’s cloud backlog and rising enterprise demand suggest this growth story may still be in its early innings.

If AI improves monetization across its ecosystem, Alphabet may deliver a powerful combination of steadier growth and multiple expansion.

TODAY’S SPONSOR

Turn AI into Your Income Engine

Ready to transform artificial intelligence from a buzzword into your personal revenue generator

HubSpot’s groundbreaking guide "200+ AI-Powered Income Ideas" is your gateway to financial innovation in the digital age.

Inside you'll discover:

A curated collection of 200+ profitable opportunities spanning content creation, e-commerce, gaming, and emerging digital markets—each vetted for real-world potential

Step-by-step implementation guides designed for beginners, making AI accessible regardless of your technical background

Cutting-edge strategies aligned with current market trends, ensuring your ventures stay ahead of the curve

Download your guide today and unlock a future where artificial intelligence powers your success. Your next income stream is waiting.

Conclusion

Nvidia remains one of the market’s most extraordinary AI businesses, but its premium valuation and cyclical exposure make the risk profile more demanding.

Alphabet offers a more balanced investment case, combining AI growth, business diversification, and stronger long-term predictability.

For investors deploying fresh capital today, Alphabet looks like the better buy right now.

Final Thought

The most rewarding AI investment may not always be the company growing the fastest, but the one built to keep winning through every cycle.

When the excitement cools and fundamentals matter most, Alphabet may be the stock better equipped to outperform over the long haul.

Can I ask a small favor from you if you find the content useful to you? Spread the wealth by sharing my FREE Newsletter with fellow stock investors and friends and help to check out my sponsor advertisement and that will keep me writing more stocks newsletters!

Of course, you should always do your own research and due diligence before investing in any stock. You should also diversify your portfolio and balance your risk and reward too!

~ Final Thought: "Fortune Favors the Bold: Embrace Opportunity Property, Execute Strategy, and Reap the Rewards of Investing Wisely.”🌱

What's Your Take on Our Newsletter? 🌟We're eager to hear your thoughts so we can make our newsletter even more amazing for you! |

Disclaimer: The content provided on this blog is for educational and informational purposes only and is not intended as financial, investment, tax, or legal advice. Investing in the stock market involves risks, including the loss of principal. The views, thoughts, and opinions expressed in this blog are solely those of the author and do not reflect the views of any company, organization, or other group. Readers are encouraged to perform their own research and due diligence before making any financial decisions and actions based on the content. Neither the author nor the publisher is liable for any losses or damages arising from the use of the advice or information contained herein.

Reply