- StocksGeniusMastery

- Posts

- 💥Nvidia Near Record Highs — Why This AI Giant Still Has Wall Street’s Attention

💥Nvidia Near Record Highs — Why This AI Giant Still Has Wall Street’s Attention

Explosive AI demand keeps lifting fundamentals, but valuation pressure is entering a new phase.

Bensheares Parker

April 26, 2026

In partnership with

Hi Fellow Investors,

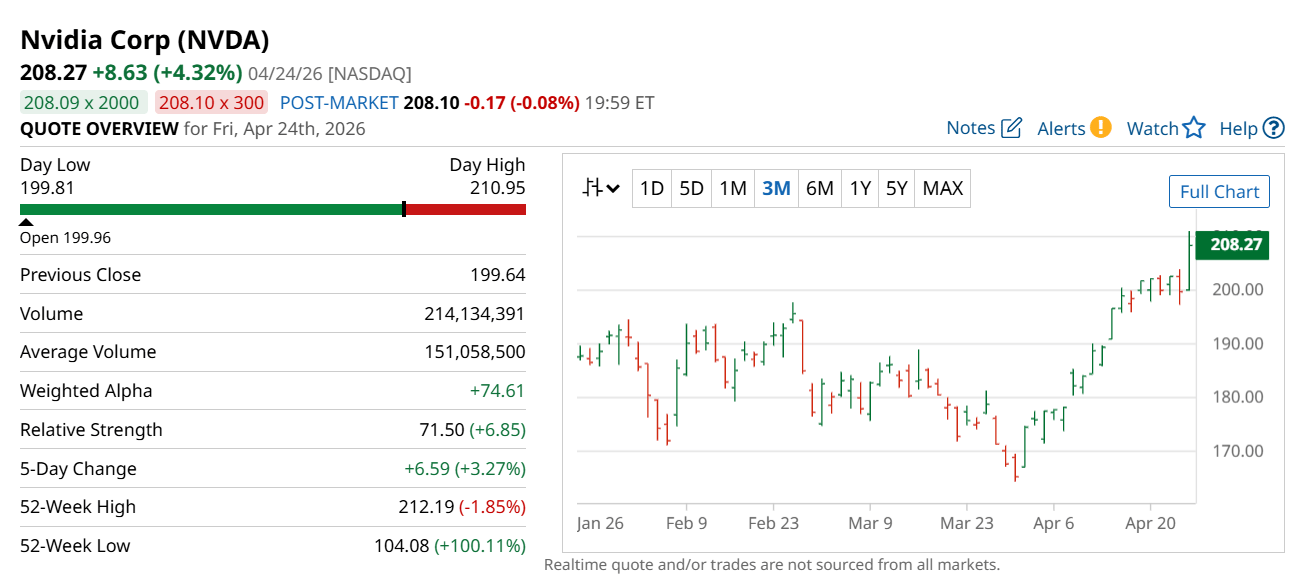

Nvidia (NASDAQ: NVDA) continues to dominate global AI investing as market value approaches an unprecedented new scale.

Revenue acceleration and industry-wide supply pressure are strengthening the bullish case again.

Even near record highs, Nvidia still commands serious long-term investor attention.

Key Points:

Nvidia’s growth accelerated again, with recent quarterly revenue expanding at 73%.

AI infrastructure spending from hyperscalers continues to support extraordinary demand.

Valuation remains elevated, but earnings momentum still justifies premium pricing.

TODAY’S SPONSOR

Talk to your AI tools the way you'd talk to a colleague.

You don't send a colleague a three-word brief. You explain the context, the constraints, what you've already tried. But typing all that into ChatGPT takes forever — so you don't.

Wispr Flow lets you speak your prompts instead. Talk through your thinking naturally and get clean, paste-ready text. No filler words. No cleanup. Just detailed prompts that actually get you useful answers on the first try.

Millions of users worldwide. Works system-wide on Mac, Windows, and iPhone.

Nvidia’s $5 Trillion Scale Reflects More Than Just Market Excitement

Nvidia now stands near the $5 trillion market capitalization threshold because its earnings power continues expanding faster than most mega-cap companies in history.

Semiconductor momentum has accelerated sharply as geopolitical concerns eased and capital spending confidence returned.

The broader chip sector has rallied aggressively, yet Nvidia remains the central profit engine behind AI infrastructure.

Its data-center leadership still defines the direction of institutional capital across semiconductors.

Very few companies at this size continue showing this level of operational acceleration.

AI Demand Is Still Expanding Faster Than Supply

The strongest part of Nvidia’s current bull case remains supply-demand imbalance.

Major hyperscalers are expected to deploy enormous capital expenditure budgets this year, much of it flowing directly into advanced compute hardware.

That spending environment continues favoring Nvidia because alternatives remain operationally weaker at scale.

Chip shortages are also reinforcing pricing discipline across the ecosystem.

This keeps Nvidia in a rare position where premium valuation still aligns with visible demand.

Margins and Ecosystem Strength Continue to Protect Nvidia’s Moat

Revenue growth of 73% confirms that Nvidia is not simply benefiting from hype but from expanding monetization across its ecosystem.

Its CUDA software advantage still gives the company a structural edge competitors have not meaningfully broken.

Gross margins remain exceptionally strong, reflecting pricing power rarely seen in hardware businesses.

The upcoming Rubin platform may create another premium upgrade cycle beyond Blackwell.

That layered ecosystem remains one of Nvidia’s strongest defenses against future competition.

Why Some Investors Still Hesitate at This Level

At nearly $5 trillion in value, future doubling becomes mathematically harder.

The semiconductor industry also has a long history of cyclical reversals after periods of exceptional demand.

Competitive pressure from custom silicon at Amazon, Alphabet, and AMD remains a medium-term factor investors cannot ignore.

If AI infrastructure spending normalizes faster than expected, sentiment could cool rapidly.

Scale itself now becomes part of the investment debate.

Strengths

Nvidia still controls the most important AI compute layer in global infrastructure spending.

Revenue acceleration at this size remains exceptionally rare and reinforces premium valuation.

CUDA continues functioning like a software lock-in advantage rather than a normal chip feature.

Weaknesses

A $5 trillion valuation naturally compresses future upside relative to smaller semiconductor names.

Semiconductor cycles historically reverse sharply after peak demand phases.

Investor expectations are now so high that even strong execution can trigger volatility.

Potential

Rubin could unlock another major earnings expansion cycle beginning in late 2026.

If AI demand keeps outpacing supply, current valuation may still look conservative in hindsight.

Enterprise AI adoption outside hyperscalers could open an entirely new growth layer.

TODAY’S SPONSOR

The summit for marketers who are tired of guessing.

Search has changed more in the last 18 months than the previous decade. Most teams are still running yesterday's playbook.

The Agentic Marketing Summit changes that. 3x Inc 5000 founder and search expert Manick Bhan breaks down the exact science behind getting found online.

Real Experts. Live. One week only.

Conclusion

Nvidia remains one of the strongest businesses in global markets today.

Its moat, pricing power, and demand visibility still support a long-term bullish stance.

The key debate is no longer business quality, but how much upside remains at extraordinary scale.

Final Thought

Great companies do not always become poor investments at high prices.

Sometimes they simply require stronger patience and sharper timing.

Can I ask a small favor from you if you find the content useful to you? Spread the wealth by sharing my FREE Newsletter with fellow stock investors and friends and help to check out my sponsor advertisement and that will keep me writing more stocks newsletters!

Of course, you should always do your own research and due diligence before investing in any stock. You should also diversify your portfolio and balance your risk and reward too!

~ Final Thought: "Fortune Favors the Bold: Embrace Opportunity Property, Execute Strategy, and Reap the Rewards of Investing Wisely.”🌱

What's Your Take on Our Newsletter? 🌟We're eager to hear your thoughts so we can make our newsletter even more amazing for you! |

Disclaimer: The content provided on this blog is for educational and informational purposes only and is not intended as financial, investment, tax, or legal advice. Investing in the stock market involves risks, including the loss of principal. The views, thoughts, and opinions expressed in this blog are solely those of the author and do not reflect the views of any company, organization, or other group. Readers are encouraged to perform their own research and due diligence before making any financial decisions and actions based on the content. Neither the author nor the publisher is liable for any losses or damages arising from the use of the advice or information contained herein.

Reply