- StocksGeniusMastery

- Posts

- 💥 Nvidia Stock in One Year: Why This AI Titan May Still Have Room to Run

💥 Nvidia Stock in One Year: Why This AI Titan May Still Have Room to Run

The multiple may shrink, but the company’s earnings expansion could still drive meaningful gains.

Bensheares Parker

April 02, 2026

Sponsored by

Hi Fellow Investors,

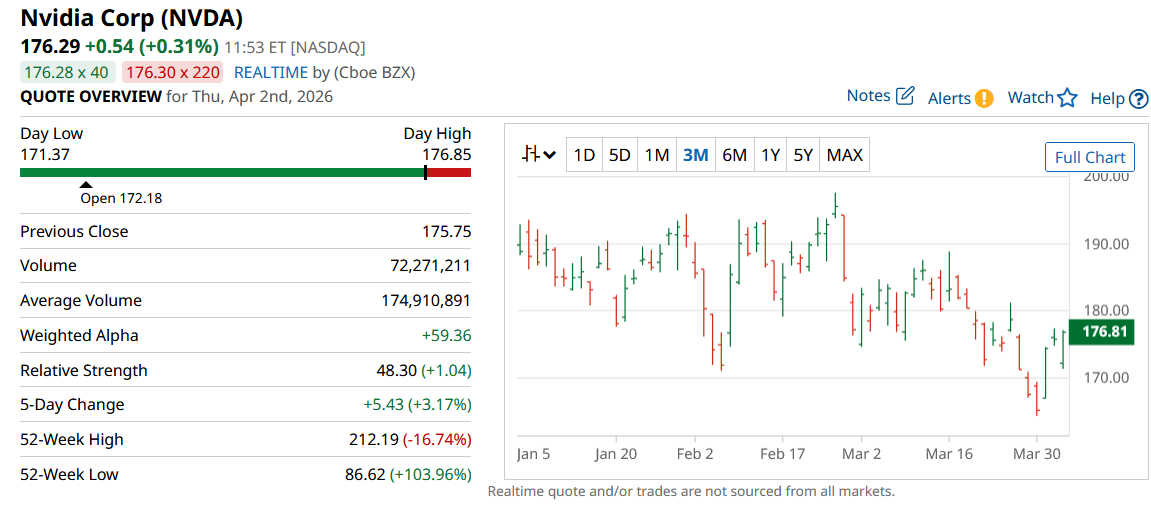

Nvidia (NASDAQ: NVDA) continues to dominate the AI infrastructure boom as revenue, profits, and investor expectations all move higher.

The real debate is no longer whether the business is thriving, but how much of that momentum can still translate into future stock gains.

Key Points:

Nvidia’s latest quarter showed extraordinary momentum, with revenue up 73% year over year and data center sales once again leading the charge.

Management’s $78 billion revenue target for the current quarter suggests the AI expansion story is still accelerating rather than slowing.

Even if Nvidia’s valuation multiple cools, the company’s earnings power could still support a plausible one-year stock price target near $197.

TODAY’S SPONSOR

How Jennifer Aniston’s LolaVie brand grew sales 40% with CTV ads

The DTC beauty category is crowded. To break through, Jennifer Aniston’s brand LolaVie, worked with Roku Ads Manager to easily set up, test, and optimize CTV ad creatives. The campaign helped drive a big lift in sales and customer growth, helping LolaVie break through in the crowded beauty category.

AI Demand Is Still Fueling a Historic Growth Engine

Nvidia’s latest quarterly report made it clear that the company is still operating at a scale few businesses in the market can match.

Fourth-quarter revenue climbed 73% year over year to $68.1 billion, showing that demand for AI infrastructure remains exceptionally strong.

Its data center segment was again the primary growth engine, generating a record $62.3 billion in revenue and rising 75% from the prior-year period.

Sequential growth was also impressive, with total revenue increasing 20% from the previous quarter.

That combination of year-over-year and quarter-over-quarter acceleration suggests Nvidia is still benefiting from a major buildout cycle across AI-capable data centers.

Management’s Outlook Suggests the AI Boom Has More Room to Run

Management’s guidance for roughly $78 billion in first-quarter revenue points to another stunning step higher in the company’s top line.

That forecast implies Nvidia’s momentum is not fading despite already massive scale.

Leadership also emphasized that the company’s data center business has expanded nearly 13-fold since fiscal 2023.

This is a striking reminder that Nvidia is not simply riding a short-lived burst of enthusiasm.

It is benefiting from a structural shift toward agentic AI, physical AI, and accelerated computing infrastructure.

Why a Lower Valuation Could Still Support a Higher Stock Price

Nvidia’s valuation looks expensive on trailing earnings, but the picture changes quickly when future profits are considered.

The stock currently trades at about 36 times earnings, yet its forward price-to-earnings ratio falls to around 21 based on expected profits over the next four quarters.

That gap matters because it shows how rapidly the company’s earnings base is expanding.

If Nvidia merely meets those forward expectations, the stock could still appreciate around 12% over the next year.

That would place shares near $197 while simultaneously making the stock look less expensive on a trailing basis than it does today.

The Risks Are Real, but the Business Still Looks Strong Enough to Push Higher

Investors should still expect valuation compression over time as growth normalizes and the market begins looking further into fiscal 2028 and beyond.

Semiconductor cycles remain real, hyperscalers will not spend at this pace forever, and rivals are aggressively pursuing custom silicon and alternative AI hardware.

Those pressures will likely force the market to assign Nvidia a more conservative earnings multiple over time.

Even so, a falling multiple does not automatically mean a falling share price when profits are rising this quickly.

With strong margins, massive cash generation, and a robust near-term pipeline, a one-year stock price target around $197 looks like a plausible outcome, even though the stock remains high risk.

Strengths

Nvidia is still delivering jaw-dropping revenue growth at enormous scale, which is a rare combination that keeps investor confidence elevated.

Its data center dominance and deep AI ecosystem create a competitive moat that remains difficult for rivals to challenge quickly.

Blackwell momentum and premium gross margins show that demand is not only strong, but also highly profitable.

Weaknesses

The stock still carries elevated expectations, which leaves little room for execution missteps or sudden demand slowdowns.

Nvidia remains exposed to the cyclical nature of semiconductors, even if the current AI cycle has been unusually powerful.

A premium valuation can compress sharply when the market starts pricing in slower future growth.

Potential

If Nvidia continues meeting or beating forward earnings estimates, the stock could climb meaningfully even as the valuation multiple cools.

Agentic AI, physical AI, and next-generation data center expansion could unlock another leg of demand that extends the growth story further.

A move toward roughly $197 over the next year looks achievable if current earnings momentum stays intact and the AI buildout remains aggressive.

TODAY’S SPONSOR

AI Alone Can’t Run Revenue

Finance doesn’t run on “mostly right.” It runs on math.

In The Architecture Behind AI-Native Revenue Automation, Tabs’s CTO breaks down why LLMs alone aren’t enough—and what it actually takes to build audit-ready, AI-driven contract-to-cash systems for modern B2B teams.

Conclusion

Nvidia still looks like one of the most powerful earnings machines in the market, and that strength could continue to support a higher stock price over the next 12 months.

The biggest takeaway is that multiple compression does not have to derail shareholder returns when profit growth remains this strong.

For investors willing to accept elevated risk, Nvidia still appears positioned to benefit from one of the most important technology buildouts of this era.

Final Thought

The biggest winners in the market are often the companies whose fundamentals grow faster than the fears surrounding their valuations.

The key question now is whether Nvidia’s AI leadership can stay strong long enough to make today’s premium look surprisingly reasonable in hindsight.

Can I ask a small favor from you if you find the content useful to you? Spread the wealth by sharing my FREE Newsletter with fellow stock investors and friends and help to check out my sponsor advertisement and that will keep me writing more stocks newsletters!

Of course, you should always do your own research and due diligence before investing in any stock. You should also diversify your portfolio and balance your risk and reward too!

~ Final Thought: "Fortune Favors the Bold: Embrace Opportunity Property, Execute Strategy, and Reap the Rewards of Investing Wisely.”🌱

What's Your Take on Our Newsletter? 🌟We're eager to hear your thoughts so we can make our newsletter even more amazing for you! |

Disclaimer: The content provided on this blog is for educational and informational purposes only and is not intended as financial, investment, tax, or legal advice. Investing in the stock market involves risks, including the loss of principal. The views, thoughts, and opinions expressed in this blog are solely those of the author and do not reflect the views of any company, organization, or other group. Readers are encouraged to perform their own research and due diligence before making any financial decisions and actions based on the content. Neither the author nor the publisher is liable for any losses or damages arising from the use of the advice or information contained herein.

Reply