- StocksGeniusMastery

- Posts

- 💥Nvidia vs. Broadcom: Which AI Giant Offers Better Upside Right Now?

💥Nvidia vs. Broadcom: Which AI Giant Offers Better Upside Right Now?

Diverging views on valuation and AI demand are creating one of 2026’s most important semiconductor debates.

Bensheares Parker

April 06, 2026

In partnership with

Hi Fellow Investors,

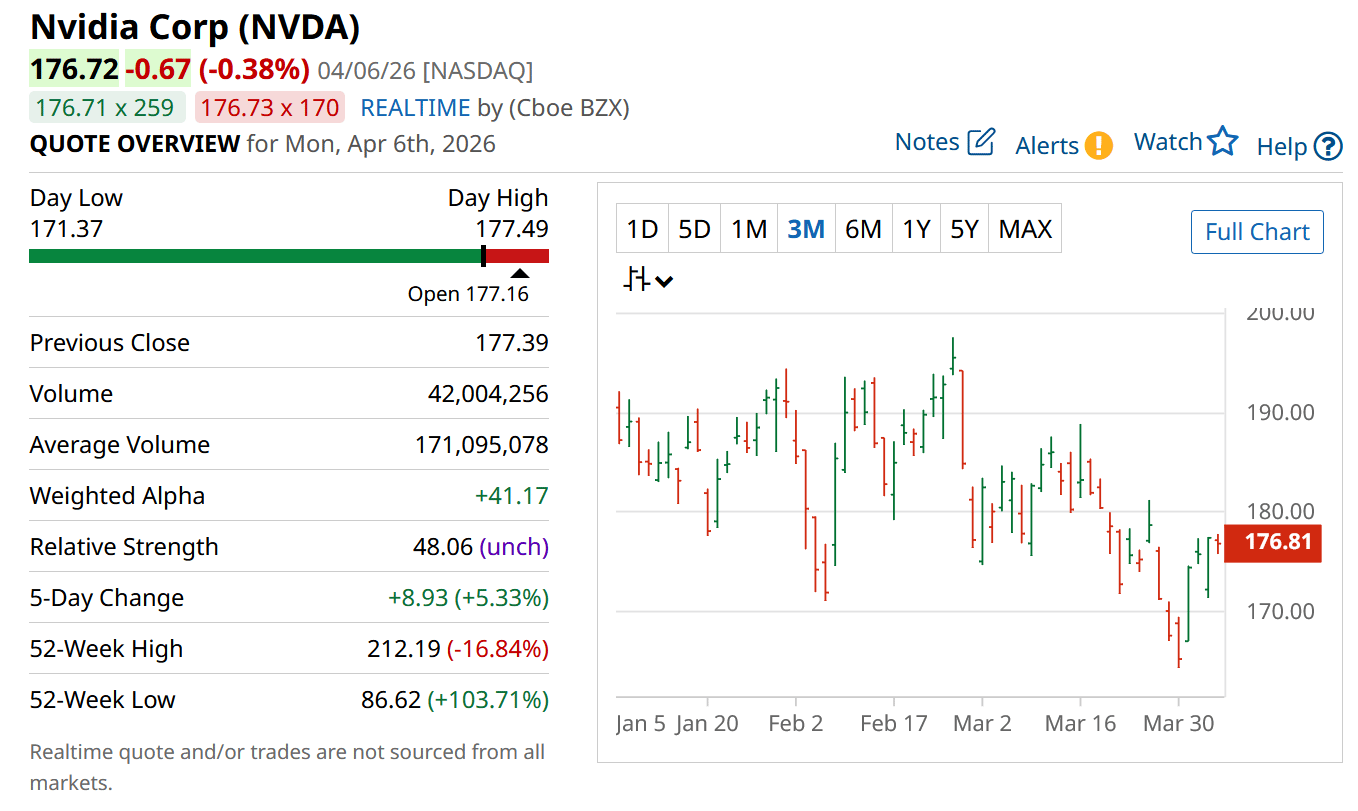

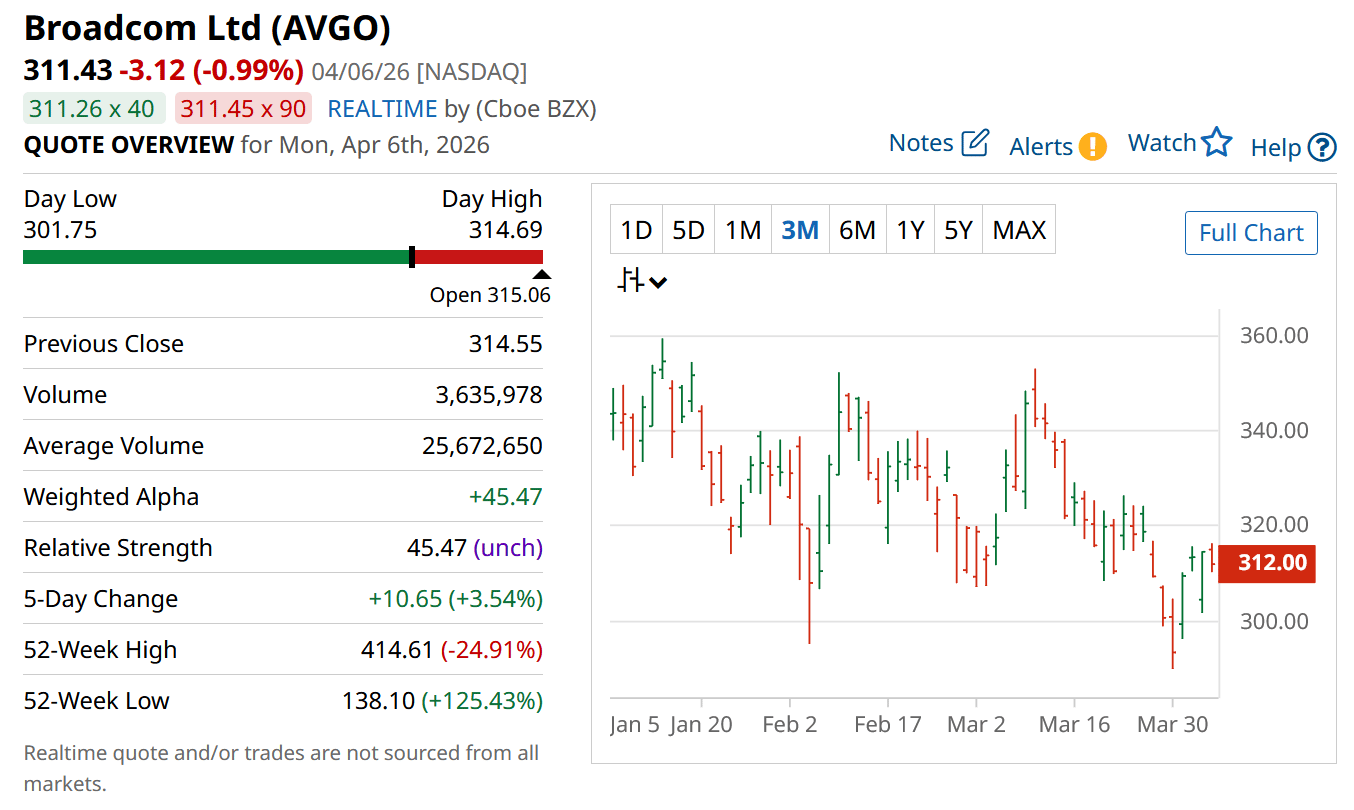

NVIDIA Corporation (NASDAQ: NVDA) and Broadcom Inc. (NASDAQ: AVGO) remain two of the most important infrastructure players in artificial intelligence, but Wall Street is increasingly debating how their next phase of upside should be valued.

One rare analyst downgrade has added fresh fuel to a debate that now centers on durability, valuation, and competitive structure.

Key Points:

Nvidia still dominates AI compute through GPUs and software, but skepticism is emerging around circular demand and custom silicon risks.

Broadcom is rapidly scaling AI networking and custom accelerator revenue while benefiting from major hyperscaler partnerships.

Both remain strong long-term businesses, but their paths to upside now depend on very different execution drivers.

TODAY’S SPONSOR

Ship Docs Your Team Is Actually Proud Of

Mintlify helps you create fast, beautiful docs that developers actually enjoy using. Write in markdown, sync with your repo, and deploy in minutes. Built-in components handle search, navigation, API references, and interactive examples out of the box, so you can focus on clear content instead of custom infrastructure.

Automatic versioning, analytics, and AI powered search make it easy to scale as your product grows. Your docs stay accurate automatically with AI-powered workflows with every pull request.

Whether you're a dev, technical writer, part of devrel, and beyond, Mintlify fits into the way you already work and helps your documentation keep pace with your product.

Why Nvidia Still Commands the Strongest Position in AI Infrastructure

Nvidia remains the global benchmark for AI accelerators because its GPUs continue setting performance standards across both training and inference workloads.

Its biggest advantage still goes beyond hardware because CUDA remains deeply embedded across enterprise and cloud AI development.

That software moat gives Nvidia a level of ecosystem control that most semiconductor competitors cannot replicate.

Even large hyperscalers using internal chips still rely heavily on Nvidia infrastructure for broad AI deployment.

This keeps Nvidia strategically central even as alternative architectures expand.

Why Some Analysts Are Starting to Question Nvidia’s Demand Model

The rare bearish view centers on whether some of Nvidia’s ecosystem spending artificially reinforces near-term demand.

Large cloud service agreements and strategic investments in AI companies have led critics to question whether portions of demand are indirectly self-supported.

Bears argue that equity stakes in firms such as Anthropic and OpenAI may blur pure end-market demand visibility.

Others see those moves as ecosystem building that strengthens Nvidia’s long-term platform dominance.

The market now watches carefully to determine whether demand remains organically strong as deployment matures.

Nvidia’s Earnings Still Argue Against the Bear Case

Despite skepticism, Nvidia’s latest financial results remain exceptionally strong.

Adjusted earnings rose 82% in the latest quarter, showing acceleration rather than deceleration.

Consensus still expects annual earnings growth above 50% through fiscal 2028.

At roughly 37 times earnings, that multiple remains demanding but not extreme relative to growth.

For many investors, earnings strength still outweighs the current criticism.

Strengths

Nvidia still controls the most powerful AI software-and-hardware ecosystem in the industry.

CUDA continues creating deep customer dependence that protects market leadership.

Earnings growth remains unusually strong even at massive scale.

Weaknesses

Strategic customer investments create debate around how durable some demand truly is.

Premium expectations leave little room for major execution errors.

Custom silicon adoption at hyperscalers remains a long-term structural threat.

Potential

Rubin and future architectures could extend Nvidia’s lead further into enterprise AI deployment.

Networking and full-stack systems may open new profit layers beyond GPUs.

If growth remains above consensus, current valuation may still look conservative.

Broadcom Is Quietly Becoming Nvidia’s Most Serious AI Infrastructure Challenger

Broadcom’s AI strategy is built differently but is becoming increasingly powerful.

Its leadership in high-speed networking gives it critical exposure to scale-out AI clusters where hyperscalers need efficient data movement.

Tomahawk switches remain deeply embedded across modern data center architecture.

At the same time, Broadcom dominates custom AI accelerator development for several of the world’s largest AI customers.

That combination gives Broadcom unusual strategic leverage inside hyperscaler infrastructure budgets.

Custom Silicon Is Turning Broadcom Into a Major AI Winner

Broadcom’s custom XPU business is now expanding rapidly through partnerships with hyperscalers and frontier AI labs.

Its tensor processing work for Alphabet Inc. remains one of the most visible examples of this strength.

The company also designs custom silicon for Meta Platforms, Inc. and several major AI developers.

AI semiconductor revenue surged 106% in the latest quarter, showing that deployment is accelerating.

Management also expects further acceleration as major customer rollouts deepen.

Why Broadcom’s Growth Story Is Becoming Harder to Ignore

Broadcom still carries slower overall growth because legacy semiconductor and infrastructure software businesses remain part of the mix.

Even so, total revenue rose 29% while earnings climbed 28%.

Management expects revenue growth to accelerate sharply to 46% next quarter.

As AI becomes a larger share of revenue, legacy drag should gradually weaken.

That creates a setup where Broadcom may look increasingly like a pure AI infrastructure compounder.

Strengths

Broadcom dominates custom AI silicon and high-speed networking, two critical layers of hyperscaler deployment.

Deep customer relationships give it recurring visibility into long-term AI spending plans.

AI revenue acceleration is becoming a larger driver of total company growth.

Weaknesses

Legacy businesses still dilute headline growth compared with Nvidia.

The stock trades at a premium multiple despite slower current revenue expansion.

Broadcom’s software and legacy chip exposure can complicate valuation clarity.

Potential

If custom XPU deployment expands further, Broadcom could gain much larger AI market share than many expect.

Networking demand may accelerate as larger AI clusters require more efficient interconnect systems.

Margin leverage could improve materially as AI products become a larger portion of revenue.

TODAY’S SPONSOR

Turn AI into Your Income Engine

Ready to transform artificial intelligence from a buzzword into your personal revenue generator

HubSpot’s groundbreaking guide "200+ AI-Powered Income Ideas" is your gateway to financial innovation in the digital age.

Inside you'll discover:

A curated collection of 200+ profitable opportunities spanning content creation, e-commerce, gaming, and emerging digital markets—each vetted for real-world potential

Step-by-step implementation guides designed for beginners, making AI accessible regardless of your technical background

Cutting-edge strategies aligned with current market trends, ensuring your ventures stay ahead of the curve

Download your guide today and unlock a future where artificial intelligence powers your success. Your next income stream is waiting.

Conclusion

Nvidia still looks stronger in ecosystem dominance and valuation efficiency relative to current growth.

Broadcom, however, is emerging as the clearest structural challenger inside hyperscaler AI infrastructure.

For long-term investors, both remain attractive, but Nvidia still appears slightly better positioned if execution remains strong.

Final Thought

The AI infrastructure race may not produce a single winner because different layers of the stack are becoming equally valuable.

Sometimes the strongest long-term returns come from understanding where dominance is widening and where disruption is quietly building.

Can I ask a small favor from you if you find the content useful to you? Spread the wealth by sharing my FREE Newsletter with fellow stock investors and friends and help to check out my sponsor advertisement and that will keep me writing more stocks newsletters!

Of course, you should always do your own research and due diligence before investing in any stock. You should also diversify your portfolio and balance your risk and reward too!

~ Final Thought: "Fortune Favors the Bold: Embrace Opportunity Property, Execute Strategy, and Reap the Rewards of Investing Wisely.”🌱

What's Your Take on Our Newsletter? 🌟We're eager to hear your thoughts so we can make our newsletter even more amazing for you! |

Disclaimer: The content provided on this blog is for educational and informational purposes only and is not intended as financial, investment, tax, or legal advice. Investing in the stock market involves risks, including the loss of principal. The views, thoughts, and opinions expressed in this blog are solely those of the author and do not reflect the views of any company, organization, or other group. Readers are encouraged to perform their own research and due diligence before making any financial decisions and actions based on the content. Neither the author nor the publisher is liable for any losses or damages arising from the use of the advice or information contained herein.

Reply