- StocksGeniusMastery

- Posts

- 💥Palantir’s Next Big Move Could Surprise Investors in 2027

💥Palantir’s Next Big Move Could Surprise Investors in 2027

AI demand remains powerful, but valuation compression still shadows the stock.

Bensheares Parker

April 09, 2026

In partnership with

Hi Fellow Investors,

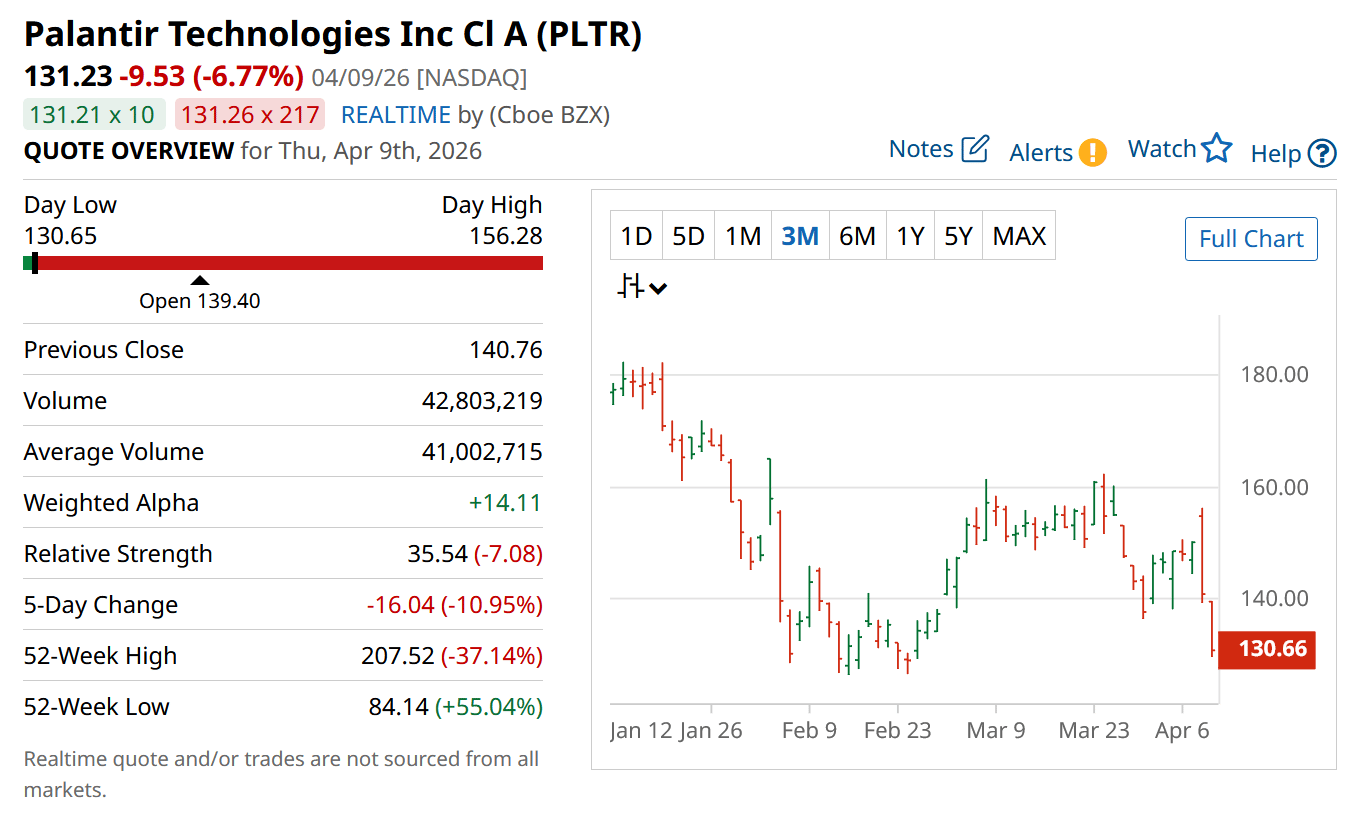

Palantir Technologies Inc. (NASDAQ: PLTR) remains one of the most debated artificial intelligence stocks because few companies combine such powerful growth with such an aggressive valuation profile.

Its recent pullback has reduced some excess enthusiasm, but the underlying operating momentum remains unusually strong.

Key Points:

Palantir continues expanding as one of the strongest enterprise AI software platforms in the market.

Earnings expectations keep rising as analysts revise forecasts upward.

A move toward $225 is possible, but valuation compression remains the central risk.

TODAY’S SPONSOR

AI Agents Are Reading Your Docs. Are You Ready?

Last month, 48% of visitors to documentation sites across Mintlify were AI agents, not humans.

Claude Code, Cursor, and other coding agents are becoming the actual customers reading your docs. And they read everything.

This changes what good documentation means. Humans skim and forgive gaps. Agents methodically check every endpoint, read every guide, and compare you against alternatives with zero fatigue.

Your docs aren't just helping users anymore. They're your product's first interview with the machines deciding whether to recommend you.

That means: clear schema markup so agents can parse your content, real benchmarks instead of marketing fluff, open endpoints agents can actually test, and honest comparisons that emphasize strengths without hype.

Mintlify powers documentation for over 20,000 companies, reaching 100M+ people every year. We just raised a $45M Series B led by @a16z and @SalesforceVC to build the knowledge layer for the agent era.

Palantir Has Built One of the Most Distinct AI Platforms in Enterprise Software

Palantir’s competitive edge comes from how its software structures decision-making rather than simply presenting analytics.

Its ontology framework creates a digital operating layer that links actions, systems, and outcomes across an organization.

That architecture makes it easier for enterprises to integrate large language models directly into operational workflows.

Instead of producing static reports, Palantir allows customers to build AI systems that actively influence decisions.

This is one reason the platform continues gaining traction in complex enterprise environments.

Why Industry Recognition Matters More Than Many Investors Realize

Recent leadership recognition in AI decisioning platforms strengthens Palantir’s enterprise credibility.

Independent validation matters because large organizations often rely heavily on third-party rankings before committing to major software deployments.

Palantir has increasingly moved from niche strategic deployments into broader enterprise adoption.

That transition expands both contract size and recurring revenue potential.

It also helps explain why financial acceleration has remained so strong.

Why a $225 Target Is Possible Even With Multiple Compression

Palantir currently trades at a valuation that remains extremely expensive by traditional standards.

A price-to-earnings ratio near 200 leaves little room for disappointment.

However, if earnings reach roughly $1.50 and valuation settles near 150 times earnings, a $225 share price becomes mathematically achievable.

That assumes both strong execution and continued investor willingness to pay a premium for growth.

The market’s tolerance for that premium remains the key unknown.

The Biggest Risk Is Still Valuation Gravity

Even exceptional businesses eventually face valuation normalization.

Palantir trades at a multiple far above the broader market, which creates structural downside if sentiment weakens.

A strong business does not always protect a stock when valuation becomes the dominant variable.

If earnings growth slows even modestly, the multiple could compress much faster than expected.

That is why valuation matters more here than with many other AI names.

Strengths

Palantir has one of the most differentiated enterprise AI software architectures in the market.

Earnings growth continues accelerating while analyst estimates keep moving higher.

Platform adoption is increasingly supported by independent enterprise software recognition.

Weaknesses

The stock remains one of the most expensive major AI names by earnings multiple.

Valuation leaves little protection if growth slows even slightly.

Market sentiment can overpower fundamentals when premium multiples are extreme.

Potential

If enterprise AI adoption continues accelerating, Palantir may sustain premium pricing longer than skeptics expect.

Government and commercial expansion could drive another wave of estimate upgrades.

Strong execution through 2026 could still justify major upside despite valuation concerns.

TODAY’S SPONSOR

88% resolved. 22% loyal. Your stack has a problem.

Those numbers aren't a CX issue — they're a design issue. Gladly's 2026 Customer Expectations Report breaks down exactly where AI-powered service loses customers, and what the architecture of loyalty-driven CX actually looks like.

Conclusion

Palantir remains one of the strongest pure software expressions of the AI trend, but valuation is inseparable from the investment case.

A move toward $225 is possible if earnings continue surprising upward and premium sentiment holds.

For now, investors are effectively betting that growth can outrun valuation gravity.

Final Thought

The most difficult stocks to value are often the ones building entirely new categories.

Palantir may continue proving that software leadership can stay expensive far longer than traditional models expect.

Can I ask a small favor from you if you find the content useful to you? Spread the wealth by sharing my FREE Newsletter with fellow stock investors and friends and help to check out my sponsor advertisement and that will keep me writing more stocks newsletters!

Of course, you should always do your own research and due diligence before investing in any stock. You should also diversify your portfolio and balance your risk and reward too!

~ Final Thought: "Fortune Favors the Bold: Embrace Opportunity Property, Execute Strategy, and Reap the Rewards of Investing Wisely.”🌱

What's Your Take on Our Newsletter? 🌟We're eager to hear your thoughts so we can make our newsletter even more amazing for you! |

Disclaimer: The content provided on this blog is for educational and informational purposes only and is not intended as financial, investment, tax, or legal advice. Investing in the stock market involves risks, including the loss of principal. The views, thoughts, and opinions expressed in this blog are solely those of the author and do not reflect the views of any company, organization, or other group. Readers are encouraged to perform their own research and due diligence before making any financial decisions and actions based on the content. Neither the author nor the publisher is liable for any losses or damages arising from the use of the advice or information contained herein.

Reply