- StocksGeniusMastery

- Posts

- 💥 The GLP-1 Gold Rush May Be Peaking for Eli Lilly

💥 The GLP-1 Gold Rush May Be Peaking for Eli Lilly

What Novo Nordisk’s pill means for long-term investors.

Bensheares Parker

January 15, 2026

In partnership with

Hi Fellow Investors,

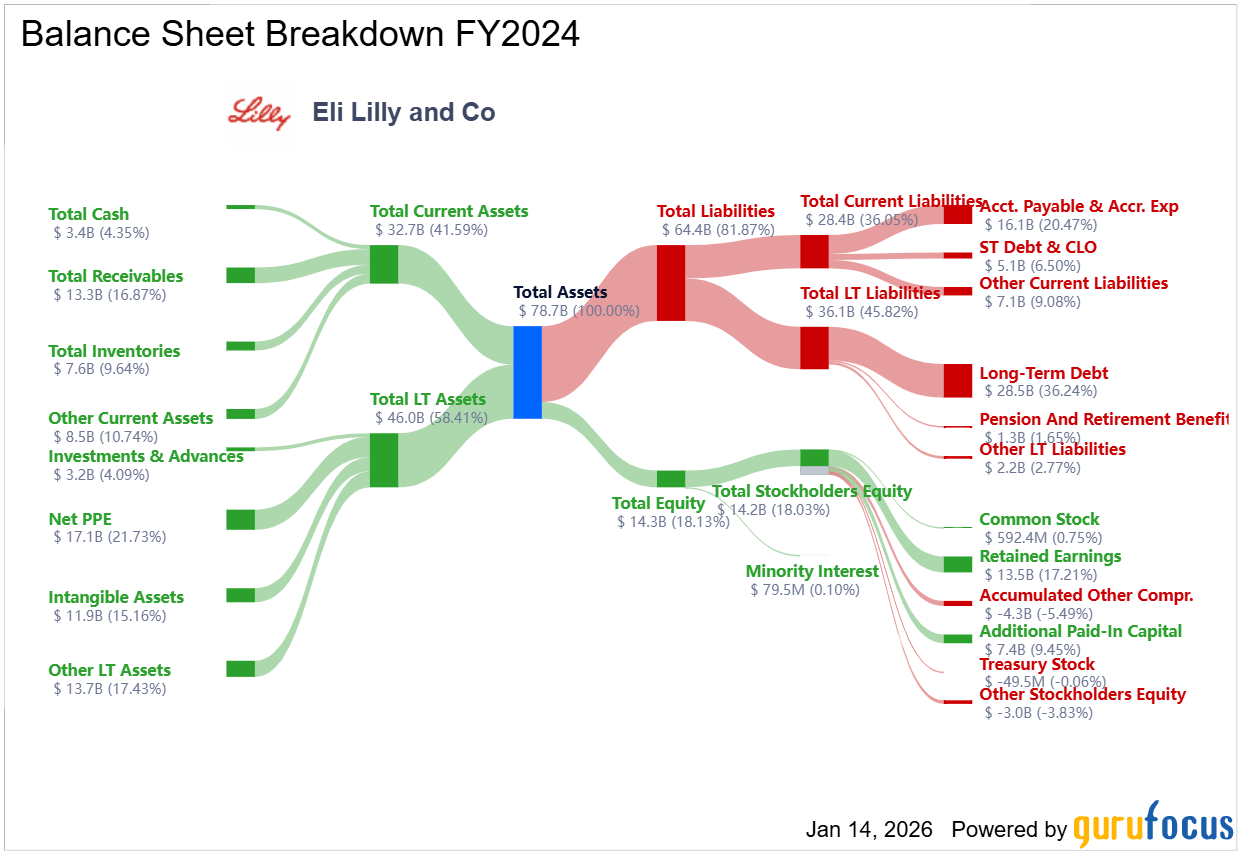

Eli Lilly (NYSE: LLY) has delivered extraordinary returns over the past five years.

That performance has been fueled almost entirely by dominance in the GLP-1 weight-loss drug market.

However, shifting competition and valuation pressures are forcing investors to reassess future upside.

Key Points:

Eli Lilly’s GLP-1 drugs Mounjaro and Zepbound now generate more than half of company revenue.

Novo Nordisk’s new pill-based GLP-1 drug threatens Lilly’s injection-based dominance.

Eli Lilly trades at a premium valuation that leaves little margin for error.

TODAY’S SPONSOR

Hiring in 8 countries shouldn't require 8 different processes

This guide from Deel breaks down how to build one global hiring system. You’ll learn about assessment frameworks that scale, how to do headcount planning across regions, and even intake processes that work everywhere. As HR pros know, hiring in one country is hard enough. So let this free global hiring guide give you the tools you need to avoid global hiring headaches.

Eli Lilly’s GLP-1 Success Is Both a Strength and a Risk

Eli Lilly’s explosive growth has been powered by the massive adoption of its GLP-1 weight-loss drugs.

Mounjaro and Zepbound were second to market but quickly became category leaders due to superior outcomes and demand.

These two therapies accounted for roughly 54% of total revenue through the first nine months of 2025.

As a result, Eli Lilly posted year-over-year revenue growth of approximately 46% during that period.

However, such concentration exposes the company to outsized risk if demand dynamics change.

When growth depends heavily on only two drugs, future volatility becomes unavoidable.

Competition Is Accelerating Faster Than Investors Expected

Novo Nordisk’s introduction of a pill-based GLP-1 drug represents a meaningful shift in patient convenience.

Oral medications are often preferred over injections, particularly for long-term therapies.

This innovation could lead to market share erosion for injectable GLP-1 treatments.

Eli Lilly is developing its own pill version, but approval timelines remain uncertain.

Meanwhile, Pfizer is pursuing GLP-1 therapies and has positioned itself to distribute a competing oral option.

The GLP-1 market remains large, but Eli Lilly’s dominance is clearly under increasing pressure.

Valuation Leaves No Room for Disappointment

Eli Lilly currently trades at a price-to-earnings ratio near 52.

That multiple is well above both the broader market and the average pharmaceutical company.

Investors are effectively pricing in years of flawless execution and sustained GLP-1 leadership.

Any slowdown in growth, pricing pressure, or competitive disruption could weigh heavily on shares.

Management is attempting to mitigate future risk through acquisitions that expand the drug pipeline.

Still, valuation remains elevated relative to the risks embedded in the business model.

Strengths

Industry-leading GLP-1 drugs have established Eli Lilly as a dominant force in metabolic healthcare.

Massive cash flows from Mounjaro and Zepbound provide funding for pipeline expansion and acquisitions.

Strong execution has delivered exceptional shareholder returns and operational momentum.

Weaknesses

Revenue concentration around two drugs increases vulnerability to competitive disruption.

High valuation amplifies downside risk if growth expectations soften.

Future patent expirations could significantly reduce long-term pricing power.

Potential

Successful development of oral GLP-1 therapies could preserve market leadership.

Pipeline diversification through acquisitions may reduce reliance on weight-loss drugs.

Continued global expansion could sustain elevated revenue growth for several more years.

TODAY’S SPONSOR

We’re running a super short survey to see if our newsletter ads are being noticed. It takes about 20 seconds and there's just a few easy questions.

Your feedback helps us make smarter, better ads.

Conclusion

Eli Lilly remains one of the most successful healthcare stories of the decade.

However, rising competition and stretched valuation suggest future returns may look very different from the past.

Investors must decide whether confidence in long-term innovation outweighs near-term risk.

Final Thought

Extraordinary stocks rarely stay cheap forever.

The real question is whether Eli Lilly’s next breakthrough can justify today’s premium price.

Can I ask a small favor from you if you find the content useful to you? Spread the wealth by sharing my FREE Newsletter with fellow stock investors and friends and help to check out my sponsor advertisement and that will keep me writing more stocks newsletters!

Of course, you should always do your own research and due diligence before investing in any stock. You should also diversify your portfolio and balance your risk and reward too!

~ Final Thought: "Fortune Favors the Bold: Embrace Opportunity Property, Execute Strategy, and Reap the Rewards of Investing Wisely.”🌱

What's Your Take on Our Newsletter? 🌟We're eager to hear your thoughts so we can make our newsletter even more amazing for you! |

Disclaimer: The content provided on this blog is for educational and informational purposes only and is not intended as financial, investment, tax, or legal advice. Investing in the stock market involves risks, including the loss of principal. The views, thoughts, and opinions expressed in this blog are solely those of the author and do not reflect the views of any company, organization, or other group. Readers are encouraged to perform their own research and due diligence before making any financial decisions and actions based on the content. Neither the author nor the publisher is liable for any losses or damages arising from the use of the advice or information contained herein.

Reply