- StocksGeniusMastery

- Posts

- 💥The Next Market Cap Giants: Which AI Stocks Could Dominate by 2030?

💥The Next Market Cap Giants: Which AI Stocks Could Dominate by 2030?

Semiconductor powerhouses may soon overtake legacy megacaps as infrastructure spending explodes.

Bensheares Parker

April 10, 2026

In partnership with

Hi Fellow Investors,

NVIDIA Corporation continues to define the current AI era, but the biggest market cap winners by 2030 may include more semiconductor infrastructure names than many investors currently expect.

The next four years could reshape the global top-five list around AI spending intensity rather than legacy consumer dominance.

Key Points:

Nvidia likely remains central if global AI infrastructure spending expands toward projected trillion-dollar levels.

Broadcom Inc. and Taiwan Semiconductor Manufacturing Company could rise sharply if hyperscaler demand remains strong.

Apple Inc. and Amazon.com, Inc. may face slower relative growth in a semiconductor-led market cycle.

TODAY’S SPONSOR

This Deloitte Fast 500 Honoree Is Eyeing 7X Growth

On 55,000+ screens in the US, a new cutting-edge AI platform is modernizing the guest experience across industries.

And the company behind it, Edison Interactive, is just getting started. They’ve even opened a new investment opportunity with plans to grow its footprint from 55,000 to 400,000 screens.

Edison’s AI-powered entertainment platform modernizes screens in venues like golf courses and hotels, helping the company earn Deloitte Fast 500 Honoree. Already deployed at premier locations like TPC, Bethpage, and Caesars Entertainment, it opens new revenue streams for operators and Edison. In fact, they’ve already earned $60M to date.

And to grow its footprint 7X, Edison is doing more than just expanding in golf and hospitality. Verizon is partnering with Edison to bring their platform to professional sports stadiums. From there, airplanes, cruise ships, trains, and more await.

This is a paid advertisement for Edison Interactive Regulation CF offering. Please read the offering circular at https://invest.edisoninteractive.com/

Why Nvidia Still Looks Positioned to Stay at the Top

Nvidia (NASDAQ: NVDA) remains the most direct beneficiary of AI infrastructure expansion because it controls the highest-value layer of accelerated compute.

Its GPU leadership still shapes spending decisions across nearly every hyperscaler and frontier AI lab.

If annual data center capital expenditures move toward multi-trillion-dollar levels, Nvidia’s revenue base could expand far beyond current consensus assumptions.

The company also continues extending its influence through networking, CPUs, and full-stack compute systems.

That combination makes it difficult to displace at the top of the market cap rankings.

Why Alphabet and Microsoft Still Look Secure in the AI Era

Alphabet Inc. (NASDAQ: GOOGL) and Microsoft Corporation (NASDAQ: MSFT) remain strongly positioned because AI demand increasingly monetizes through cloud infrastructure.

Google Cloud and Azure are both showing unusually strong growth tied to enterprise AI workloads.

As AI deployment deepens, cloud platforms become direct earnings beneficiaries rather than indirect participants.

That gives both companies a second growth engine beyond their traditional software and digital businesses.

Their scale and free cash generation make their top-five positions difficult to challenge.

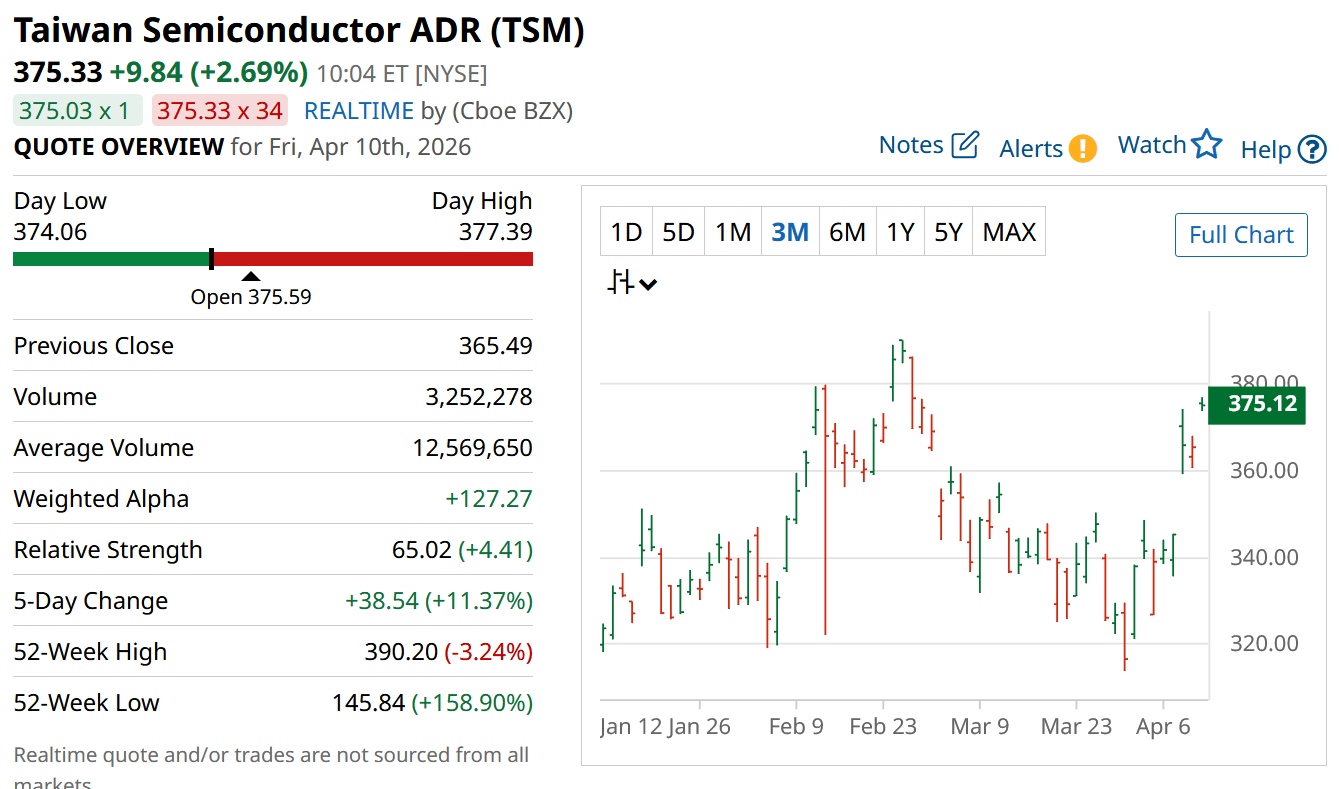

Why Taiwan Semiconductor Could Become One of the Biggest Winners

Taiwan Semiconductor (NYSE: TSM) sits underneath nearly every major AI hardware success story.

Its foundry dominance gives it exposure to nearly all leading-edge chip demand without depending on a single product winner.

Nvidia, Apple, and many advanced chip designers rely heavily on its manufacturing leadership.

As AI chips become more complex, advanced node demand strengthens Taiwan Semiconductor’s pricing and strategic leverage.

That makes it one of the clearest long-duration beneficiaries of infrastructure expansion.

Strengths

Taiwan Semiconductor controls the most critical advanced manufacturing layer in global semiconductors.

AI demand expands revenue visibility across many customers simultaneously.

Leading-edge process leadership remains extremely difficult for competitors to replicate.

Weaknesses

Geopolitical risk always remains part of the investment case.

Capital intensity requires constant execution and enormous reinvestment.

Revenue still depends on customer product cycles beyond its direct control.

Potential

AI chip complexity may expand margins further as advanced packaging becomes more valuable.

Foundry demand could remain structurally elevated through the next decade.

If AI spending reaches projected levels, Taiwan Semiconductor’s scale could rise dramatically.

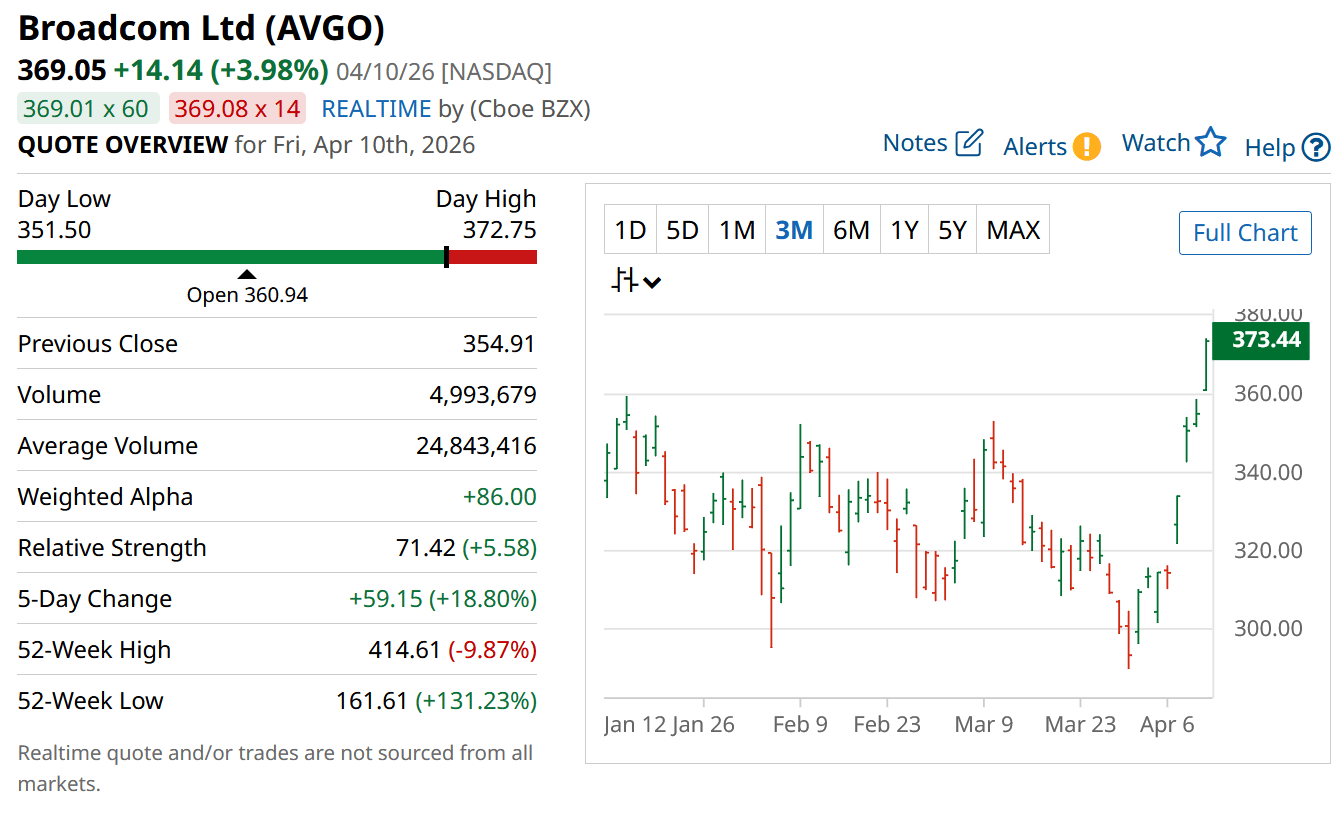

Why Broadcom Could Quietly Enter the Global Elite

Broadcom (NASDAQ: AVGO) is becoming increasingly important because AI infrastructure needs more than GPUs.

Its networking leadership remains essential for large AI clusters where data movement becomes critical.

At the same time, custom AI accelerators are creating a second major growth engine.

Broadcom now supplies highly specialized silicon for several hyperscalers and major AI developers.

That dual exposure gives it unusually broad leverage across AI deployment.

Strengths

Broadcom dominates high-speed networking and custom AI silicon simultaneously.

Deep hyperscaler relationships create unusually strong revenue visibility.

AI products are becoming a larger percentage of total growth.

Weaknesses

Legacy businesses still dilute headline growth.

Premium valuation requires continued acceleration.

AI market share gains must continue to justify future rerating.

Potential

Custom AI chips could become one of the largest semiconductor growth categories by 2030.

Networking demand may expand sharply as AI clusters scale.

Broadcom could re-rate significantly if AI becomes the dominant earnings driver.

Why Apple and Amazon May Lose Relative Position

Apple (NASDAQ: AAPL) still generates enormous profits, but its AI monetization path remains less direct than semiconductor or cloud leaders.

Its hardware growth profile also remains slower than infrastructure-led names.

Amazon (NASDAQ: AMZN) still benefits from cloud exposure through AWS, but retail continues diluting overall growth.

AWS also currently trails the acceleration seen in Azure and Google Cloud.

That does not imply weak businesses, but relative growth may no longer support top-five leadership.

TODAY’S SPONSOR

The boring Bitcoin strategy that works

Five years from now, the people who aren't stressed about markets will be the ones who did something boring today. YieldClub earns up to 12% APY and automatically routes your yield into Bitcoin, every day, whether you're watching or not.

Conclusion

The next market-cap cycle may reward infrastructure providers more than consumer ecosystems.

Semiconductors, cloud platforms, and AI networking appear positioned to drive the biggest valuation expansion.

The companies closest to AI deployment layers may ultimately control the next global hierarchy.

Final Thought

The biggest market leaders often change when technology spending shifts from consumer demand to foundational infrastructure.

This cycle increasingly looks like one where chip ecosystems may matter more than brand ecosystems.

Can I ask a small favor from you if you find the content useful to you? Spread the wealth by sharing my FREE Newsletter with fellow stock investors and friends and help to check out my sponsor advertisement and that will keep me writing more stocks newsletters!

Of course, you should always do your own research and due diligence before investing in any stock. You should also diversify your portfolio and balance your risk and reward too!

~ Final Thought: "Fortune Favors the Bold: Embrace Opportunity Property, Execute Strategy, and Reap the Rewards of Investing Wisely.”🌱

What's Your Take on Our Newsletter? 🌟We're eager to hear your thoughts so we can make our newsletter even more amazing for you! |

Disclaimer: The content provided on this blog is for educational and informational purposes only and is not intended as financial, investment, tax, or legal advice. Investing in the stock market involves risks, including the loss of principal. The views, thoughts, and opinions expressed in this blog are solely those of the author and do not reflect the views of any company, organization, or other group. Readers are encouraged to perform their own research and due diligence before making any financial decisions and actions based on the content. Neither the author nor the publisher is liable for any losses or damages arising from the use of the advice or information contained herein.

Reply