- StocksGeniusMastery

- Posts

- 💥This AI Giant Looks Positioned for Another Breakout Year

💥This AI Giant Looks Positioned for Another Breakout Year

Earnings forecasts and AI infrastructure demand suggest far more upside than the market currently prices in.

Bensheares Parker

April 11, 2026

In partnership with

Hi Fellow Investors,

Nvidia Corporation (NASDAQ: NVDA) continues to deliver growth numbers that few megacap companies in history have matched, yet its stock still trades at a valuation that looks unusually restrained relative to that momentum.

The disconnect between earnings power and market pricing is becoming one of the most closely watched stories in AI investing.

Key Points:

Nvidia’s latest product cycle continues to strengthen revenue visibility across both training and inference markets.

Earnings expectations remain elevated and could still move higher as Rubin deployment expands.

A major rerating becomes possible if the market restores a higher premium multiple.

TODAY’S SPONSOR

Stack BTC while you sleep

Tired of trying to time the market? YieldClub puts your money on autopilot. Deposit from your bank account, and your balance starts earning automatically, routing yield into Bitcoin around the clock. No charts, no timing the market, no crypto expertise required.

Nvidia’s Revenue Pipeline Remains Exceptionally Strong

Nvidia closed fiscal 2026 with extraordinary momentum.

Fourth-quarter revenue surged 73% year over year to $68 billion.

Full-year revenue reached $216 billion, while annual earnings climbed 60%.

Those results would already justify strong optimism, but management’s forward product outlook suggests the next phase may be even larger.

That is why the current valuation debate has become increasingly important.

Blackwell and Rubin May Extend Nvidia’s Lead Further

The Blackwell platform remains heavily demanded across hyperscaler deployments.

Rubin now adds another major performance leap on top of that cycle.

Management expects combined Blackwell and Rubin systems to generate roughly $1 trillion across 2026 and 2027.

That projection is far above prior internal expectations and suggests stronger deployment visibility than the market previously assumed.

Few semiconductor product cycles have ever carried this level of revenue potential.

Why Rubin Changes the Earnings Story

Rubin’s efficiency gains matter because hyperscalers increasingly optimize around energy and cost.

Management indicates Rubin delivers roughly 3.5 times faster training and 5 times faster inference versus Blackwell.

Those improvements directly influence cloud economics and AI deployment budgets.

Better economics often expand demand rather than reduce hardware spending.

That dynamic could extend Nvidia’s earnings acceleration further into fiscal 2027.

Why the Current Valuation Still Looks Unusually Low

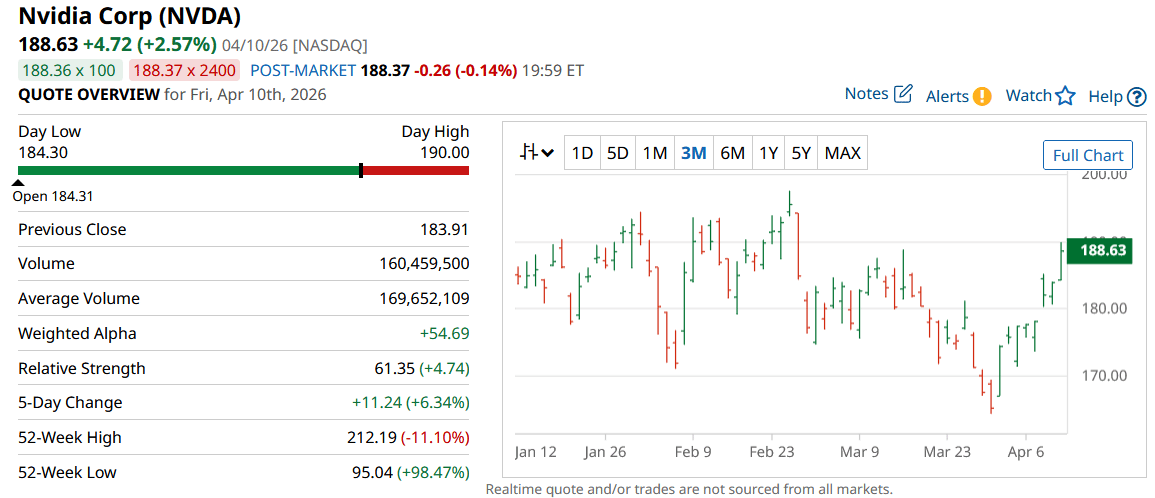

Despite this growth profile, Nvidia trades near roughly 21 times forward earnings.

That places it only slightly above the broader market multiple.

For a company with projected earnings growth near 74%, that gap looks unusually narrow.

Historically, Nvidia often traded at far richer premiums during slower growth phases.

The market currently appears more cautious than the fundamentals suggest.

Why a Major Repricing Is Plausible

If Nvidia returns to a premium multiple closer to twice the market level, the stock could move materially higher.

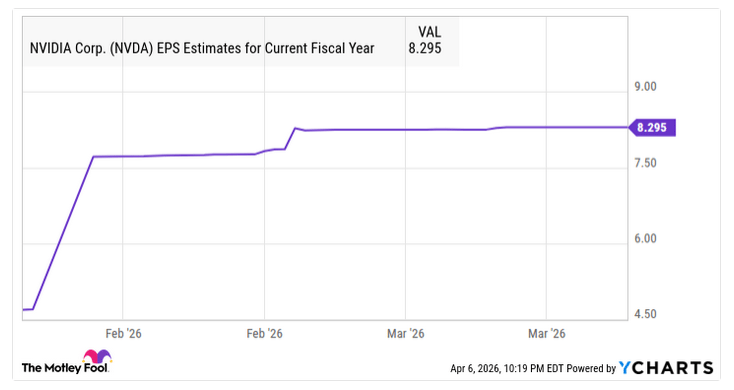

Using projected earnings near $8.29 and a multiple near 42 implies a share price near $348.

That would represent a dramatic rerating rather than an unrealistic earnings assumption.

The key variable is whether investor confidence returns as product shipments accelerate.

If that happens, valuation expansion could become the dominant driver.

Strengths

Nvidia still controls the strongest AI infrastructure ecosystem across chips, networking, and software.

Rubin and Blackwell together create one of the most powerful semiconductor revenue pipelines ever seen.

Earnings growth remains extraordinary even at megacap scale.

Weaknesses

The stock still depends on premium multiples returning for extreme upside targets to materialize.

Hyperscaler spending concentration remains a structural risk.

Macro volatility can suppress valuation despite strong operating execution.

Potential

Rubin adoption may push earnings above already aggressive consensus expectations.

Forward multiples could expand sharply if AI demand remains uninterrupted.

Nvidia may still be early in a much larger infrastructure cycle through 2030.

TODAY’S SPONSOR

Are you tracking agent views on your docs?

AI agents already outnumber human visitors to your docs — now you can track them.

Conclusion

Nvidia’s current valuation still appears conservative relative to its earnings trajectory and infrastructure leadership.

The market may eventually need to reprice the stock if execution continues at this pace.

In high-growth cycles, valuation often lags fundamentals before catching up suddenly.

Final Thought

The biggest moves in dominant technology stocks often happen when strong growth persists longer than valuation models expect.

For Nvidia, that tension still appears unresolved.

Can I ask a small favor from you if you find the content useful to you? Spread the wealth by sharing my FREE Newsletter with fellow stock investors and friends and help to check out my sponsor advertisement and that will keep me writing more stocks newsletters!

Of course, you should always do your own research and due diligence before investing in any stock. You should also diversify your portfolio and balance your risk and reward too!

~ Final Thought: "Fortune Favors the Bold: Embrace Opportunity Property, Execute Strategy, and Reap the Rewards of Investing Wisely.”🌱

What's Your Take on Our Newsletter? 🌟We're eager to hear your thoughts so we can make our newsletter even more amazing for you! |

Disclaimer: The content provided on this blog is for educational and informational purposes only and is not intended as financial, investment, tax, or legal advice. Investing in the stock market involves risks, including the loss of principal. The views, thoughts, and opinions expressed in this blog are solely those of the author and do not reflect the views of any company, organization, or other group. Readers are encouraged to perform their own research and due diligence before making any financial decisions and actions based on the content. Neither the author nor the publisher is liable for any losses or damages arising from the use of the advice or information contained herein.

Reply