- StocksGeniusMastery

- Posts

- 💥 This Magnificent Seven Stock Is Down — And Wall Street May Be Missing the Upside

💥 This Magnificent Seven Stock Is Down — And Wall Street May Be Missing the Upside

AI fears have pressured valuations, but Nvidia’s earnings story remains unusually powerful.

Bensheares Parker

March 29, 2026

In partnership with

Hi Fellow Investors,

The Magnificent Seven has lost momentum in 2026 as investors rotate away from mega-cap leadership.

That broad weakness is creating selective entry points in elite technology names.

One stock now stands out because growth remains far stronger than valuation implies.

Key Points:

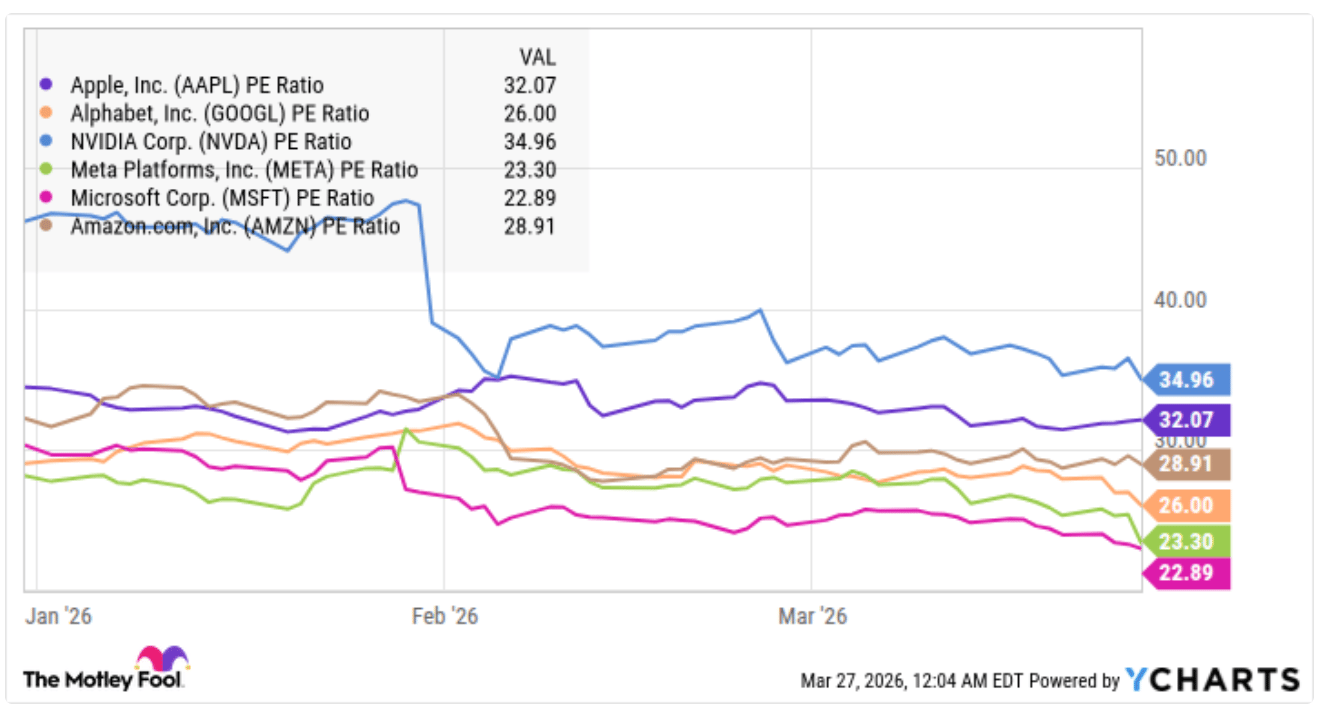

Every Magnificent Seven stock has underperformed the broader market this year.

Nvidia now trades at a forward multiple that no longer reflects hyper-growth pricing

AI infrastructure demand still strongly supports long-term earnings expansion.

TODAY’S SPONSOR

88% resolved. 22% stayed loyal. What went wrong?

That's the AI paradox hiding in your CX stack. Tickets close. Customers leave. And most teams don't see it coming because they're measuring the wrong things.

Efficiency metrics look great on paper. Handle time down. Containment rate up. But customer loyalty? That's a different story — and it's one your current dashboards probably aren't telling you.

Gladly's 2026 Customer Expectations Report surveyed thousands of real consumers to find out exactly where AI-powered service breaks trust, and what separates the platforms that drive retention from the ones that quietly erode it.

If you're architecting the CX stack, this is the data you need to build it right. Not just fast. Not just cheap. Built to last.

Why Market Rotation Is Pressuring the Biggest Tech Winners

The strongest winners of the previous bull cycle are now facing broad investor skepticism.

Capital is rotating into smaller companies as traders look for fresh upside outside mega-cap concentration.

Higher infrastructure spending across hyperscalers has raised concern about delayed returns on AI investments.

Large technology companies are now committing extraordinary capital to data center expansion.

That scale of spending has temporarily weakened sentiment across the entire sector.

Even dominant businesses are now being valued more cautiously than just months ago.

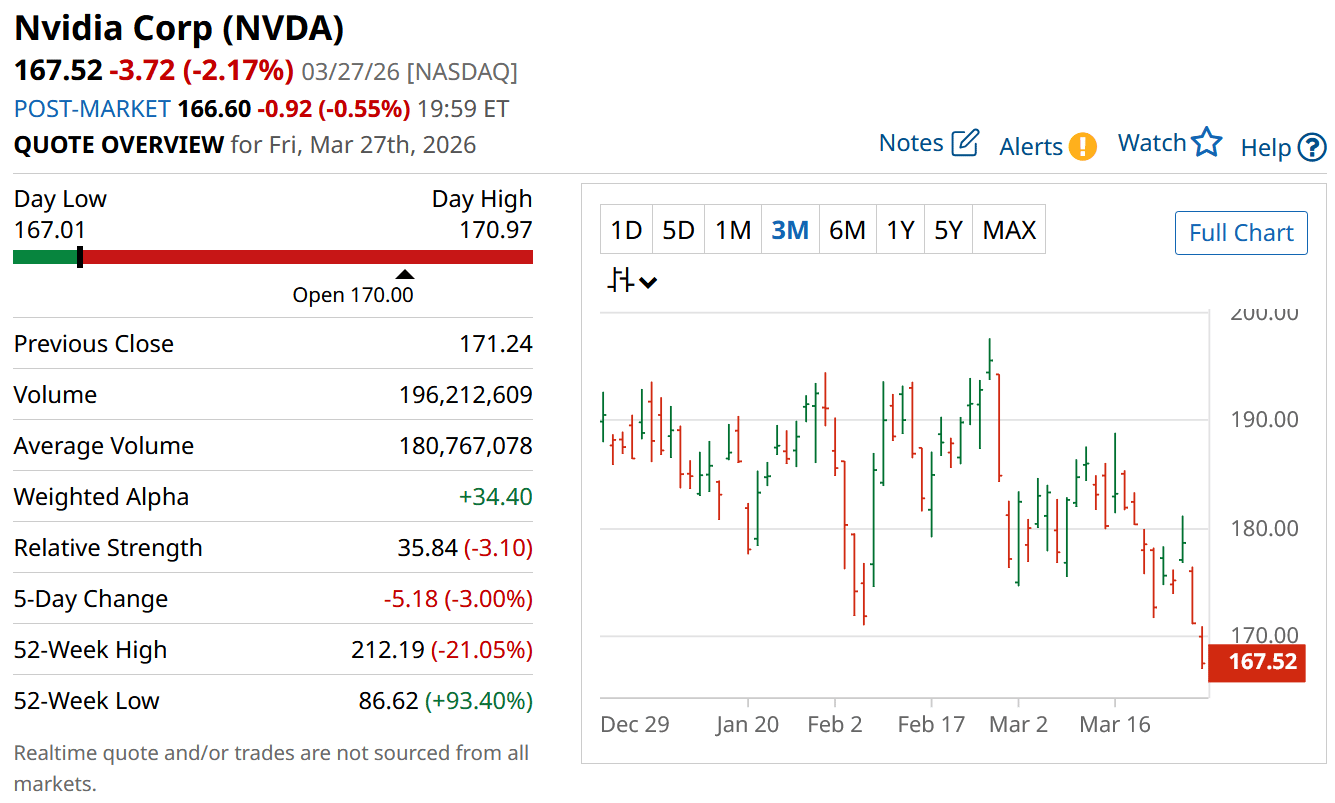

Why Nvidia Still Maintains a Structural Advantage in AI

NVIDIA (NASDAQ: NVDA) remains the central hardware supplier powering advanced AI deployment globally.

Its chips remain deeply embedded in hyperscaler spending cycles.

Demand from cloud providers continues to absorb production at extraordinary levels.

Revenue growth has recently accelerated rather than slowed.

That is highly unusual for a company already operating at massive scale.

The market is pricing Nvidia as if peak growth is near, yet reported results continue suggesting otherwise.

Why Forward Valuation Is Making Nvidia Increasingly Attractive

Although Nvidia still appears expensive on trailing earnings, forward estimates tell a different story.

Analysts expect earnings growth to remain exceptionally strong over the next fiscal periods.

That compresses the forward valuation into territory closer to broader market multiples.

A forward earnings multiple near 21 is unusually low for a company delivering sector-leading expansion.

This implies investors are heavily discounting future AI durability.

If AI demand remains persistent, current valuation may eventually look unusually conservative.

Strengths

Nvidia controls the most critical AI hardware layer across hyperscale computing.

Earnings momentum remains stronger than nearly every other mega-cap technology company.

CEO guidance continues signaling extraordinary revenue confidence.

Weaknesses

Valuation sensitivity remains high during macro-driven selloffs.

Heavy institutional ownership can amplify volatility during risk-off periods.

Geopolitical headlines may continue disrupting sentiment.

Potential

Continued hyperscaler spending could drive another major earnings revision cycle.

New enterprise AI deployments may unlock additional demand layers.

If market confidence returns, multiple expansion could accelerate quickly.

TODAY’S SPONSOR

2026’s biggest media shift

Attention is the hardest thing to buy. And everyone else is bidding too.

When people are scrolling, skipping, swiping, and split-screening their way through the day, finding uninterrupted moments where your audience is truly paying attention is the priority.

That’s where Performance TV stands out.

Check out the data from 600+ marketers on the most effective channels to capture audience attention in 2026.

Conclusion

The Magnificent Seven may be under pressure, but leadership inside that group has not disappeared.

Nvidia still combines rare earnings momentum with improving valuation support.

That combination often creates strong long-term entry opportunities.

Final Thought

The market often discounts future winners during temporary fear.

The real question is whether today’s hesitation becomes tomorrow’s missed opportunity.

Can I ask a small favor from you if you find the content useful to you? Spread the wealth by sharing my FREE Newsletter with fellow stock investors and friends and help to check out my sponsor advertisement and that will keep me writing more stocks newsletters!

Of course, you should always do your own research and due diligence before investing in any stock. You should also diversify your portfolio and balance your risk and reward too!

~ Final Thought: "Fortune Favors the Bold: Embrace Opportunity Property, Execute Strategy, and Reap the Rewards of Investing Wisely.”🌱

What's Your Take on Our Newsletter? 🌟We're eager to hear your thoughts so we can make our newsletter even more amazing for you! |

Disclaimer: The content provided on this blog is for educational and informational purposes only and is not intended as financial, investment, tax, or legal advice. Investing in the stock market involves risks, including the loss of principal. The views, thoughts, and opinions expressed in this blog are solely those of the author and do not reflect the views of any company, organization, or other group. Readers are encouraged to perform their own research and due diligence before making any financial decisions and actions based on the content. Neither the author nor the publisher is liable for any losses or damages arising from the use of the advice or information contained herein.

Reply