- StocksGeniusMastery

- Posts

- 💥This Semiconductor Giant Still Looks Undervalued Despite a Massive 2026 Surge

💥This Semiconductor Giant Still Looks Undervalued Despite a Massive 2026 Surge

Taiwan Semiconductor’s earnings strength may not yet be fully reflected in its valuation.

Bensheares Parker

April 15, 2026

In partnership with

Hi Fellow Investors,

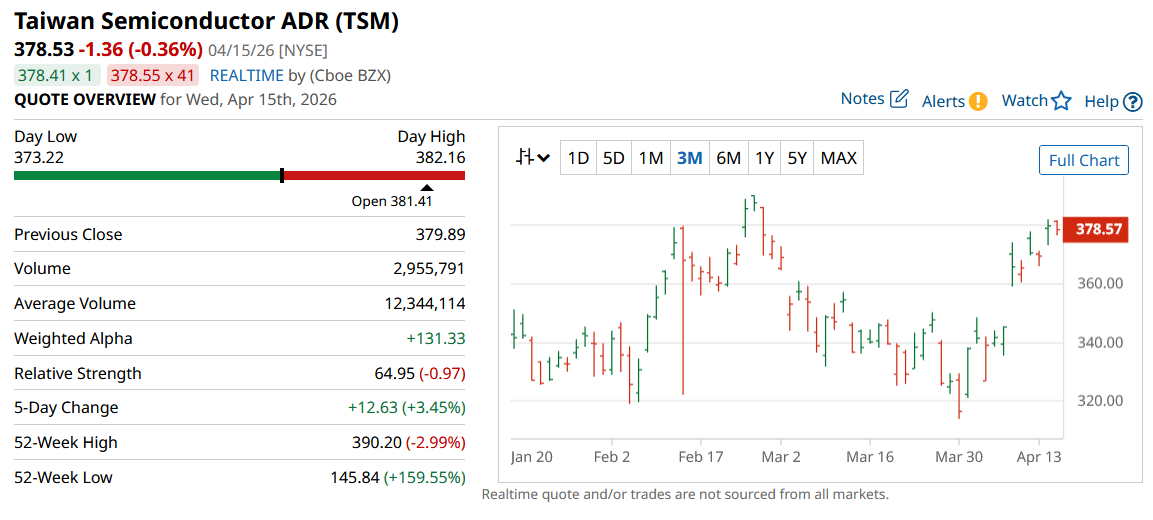

Taiwan Semiconductor Manufacturing (NYSE: TSM) continues to strengthen its position as the most critical manufacturing force behind the global semiconductor boom.

Strong first-quarter revenue has reinforced confidence that AI-driven demand remains far stronger than many investors expected entering 2026.

The approaching earnings release on April 16 could become the next major catalyst for renewed upside.

Key Points:

TSMC already exceeded first-quarter revenue guidance, signaling demand remains ahead of internal projections.

AI customers including Nvidia, AMD, and Broadcom continue expanding aggressively, directly supporting foundry utilization.

Pricing power in advanced chips may create stronger earnings acceleration than current consensus models imply.

TODAY’S SPONSOR

88% resolved. 22% stayed loyal. What went wrong?

That's the AI paradox hiding in your CX stack. Tickets close. Customers leave. And most teams don't see it coming because they're measuring the wrong things.

Efficiency metrics look great on paper. Handle time down. Containment rate up. But customer loyalty? That's a different story — and it's one your current dashboards probably aren't telling you.

Gladly's 2026 Customer Expectations Report surveyed thousands of real consumers to find out exactly where AI-powered service breaks trust, and what separates the platforms that drive retention from the ones that quietly erode it.

If you're architecting the CX stack, this is the data you need to build it right. Not just fast. Not just cheap. Built to last.

Why TSMC’s Growth Engine Still Looks Exceptionally Durable

March revenue growth accelerated sharply and pushed first-quarter sales beyond the upper end of company guidance.

That result confirms advanced-node utilization remains extremely tight across major customer segments.

TSMC continues benefiting from unmatched manufacturing scale at the highest-performance semiconductor nodes.

Its foundry leadership remains difficult for competitors to challenge because leading-edge production requires enormous technical and capital barriers.

Demand from data center chip designers has become the dominant force behind current revenue momentum.

This positions the company to keep compounding revenue even as broader technology markets remain uneven.

AI Customers Are Quietly Expanding TSMC’s Earnings Ceiling

Nvidia’s projected AI platform expansion alone suggests a far larger manufacturing pipeline ahead.

Broadcom’s expected multi-year AI chip revenue surge adds another major source of wafer demand.

AMD’s long-duration data center growth strategy further strengthens forward production visibility.

Because multiple AI leaders rely heavily on TSMC simultaneously, customer concentration now acts more as a growth amplifier than a weakness.

The company’s dominant foundry share gives it extraordinary leverage during periods of constrained advanced capacity.

That combination often leads to earnings beats when demand remains stronger than analyst assumptions.

Advanced chip pricing increases between 3% and 10% create another major earnings tailwind.

Supply remains constrained precisely where customers need the most advanced production.

That imbalance allows TSMC to defend margins while expanding profitability.

Consensus already expects strong earnings growth, yet pricing changes suggest upside may still be understated.

Forward valuation remains attractive relative to projected earnings acceleration.

This creates a rare combination of quality, momentum, and valuation support.

Strengths

TSMC controls the most critical advanced semiconductor manufacturing capacity in the world, making it indispensable to the AI supply chain.

Its 72% foundry market share creates powerful pricing leverage that few industrial companies can match.

AI demand from multiple top-tier customers provides unusually broad long-term revenue visibility.

Weaknesses

Heavy reliance on advanced-node production exposes results to any unexpected customer inventory adjustments.

Geopolitical attention around Taiwan continues to remain an unavoidable valuation discount factor.

Large-scale capital spending requirements can temporarily pressure near-term margin expansion.

Potential

A strong April 16 earnings release could trigger another institutional re-rating higher.

Continued AI chip shortages may support additional price increases through several future cycles.

Long-term earnings growth could exceed consensus if customer AI roadmaps accelerate further.

TODAY’S SPONSOR

Are You Ready to Actually Retire?

Knowing when to retire means knowing what it costs, how long your money needs to last, and where the income comes from. When to Retire: A Quick and Easy Planning Guide helps investors with $1,000,000 or more work through all of it.

Conclusion

TSMC remains one of the clearest structural winners of the AI semiconductor cycle.

Its pricing power and manufacturing dominance continue strengthening at the same time.

That combination often produces upside even after strong stock performance.

Final Thought

The market already understands TSMC is essential.

The larger opportunity may be that earnings power still has not fully caught up with how essential it has become.

Can I ask a small favor from you if you find the content useful to you? Spread the wealth by sharing my FREE Newsletter with fellow stock investors and friends and help to check out my sponsor advertisement and that will keep me writing more stocks newsletters!

Of course, you should always do your own research and due diligence before investing in any stock. You should also diversify your portfolio and balance your risk and reward too!

~ Final Thought: "Fortune Favors the Bold: Embrace Opportunity Property, Execute Strategy, and Reap the Rewards of Investing Wisely.”🌱

What's Your Take on Our Newsletter? 🌟We're eager to hear your thoughts so we can make our newsletter even more amazing for you! |

Disclaimer: The content provided on this blog is for educational and informational purposes only and is not intended as financial, investment, tax, or legal advice. Investing in the stock market involves risks, including the loss of principal. The views, thoughts, and opinions expressed in this blog are solely those of the author and do not reflect the views of any company, organization, or other group. Readers are encouraged to perform their own research and due diligence before making any financial decisions and actions based on the content. Neither the author nor the publisher is liable for any losses or damages arising from the use of the advice or information contained herein.

Reply