- StocksGeniusMastery

- Posts

- 💥 Wall Street Is Underestimating AMD: A 348% Growth Story Hiding in Plain Sight

💥 Wall Street Is Underestimating AMD: A 348% Growth Story Hiding in Plain Sight

Cheaper chips, accelerating demand, and expanding margins tell a compelling story.

Bensheares Parker

January 22, 2026

In partnership with

Hi Fellow Investors,

Advanced Micro Devices (NASDAQ: AMD) is positioning itself for a pivotal decade driven by artificial intelligence and data center expansion.

Management believes its strategic investments could unlock one of the most compelling growth stories in the semiconductor sector.

If execution matches ambition, the stock’s upside could be extraordinary.

Key Points:

Management projects data center revenue growth of 60% or more annually through 2030.

Margin expansion represents a powerful secondary catalyst for long-term stock appreciation.

Valuation is elevated, but growth and profitability improvements could justify premium pricing.

TODAY’S SPONSOR

Investor-ready updates, by voice

High-stakes communications need precision. Wispr Flow turns speech into polished, publishable writing you can paste into investor updates, earnings notes, board recaps, and executive summaries. Speak constraints, numbers, and context and Flow will remove filler, fix punctuation, format lists, and preserve tone so your messages are clear and confident. Use saved templates for recurring financial formats and create consistent reports with less editing. Works across Mac, Windows, and iPhone. Try Wispr Flow for finance.

AMD Is Rewriting Its Role in the AI Ecosystem

Advanced Micro Devices has historically been viewed as a secondary option in high-performance computing.

That narrative is beginning to shift as the company aggressively upgrades its AI-focused product lineup.

Supply constraints across the semiconductor industry are forcing customers to consider alternative vendors.

AMD’s lower-priced solutions are increasingly viewed as viable, not inferior, options.

This shift creates a rare opportunity for AMD to gain meaningful share in AI workloads.

The coming years will test whether these products can permanently change customer perception.

Data Center Growth Is the Primary Engine

Management expects data center revenue to compound at 60% annually through 2030.

That pace places AMD in the same growth conversation as the industry’s most dominant AI players.

While AMD remains diversified across client, gaming, and embedded segments, data center growth is the clear standout.

Other segments are projected to grow at a steadier 10% annual rate.

Blended together, management forecasts an overall company CAGR of roughly 35%.

Sustained execution at that level would dramatically reshape AMD’s revenue base.

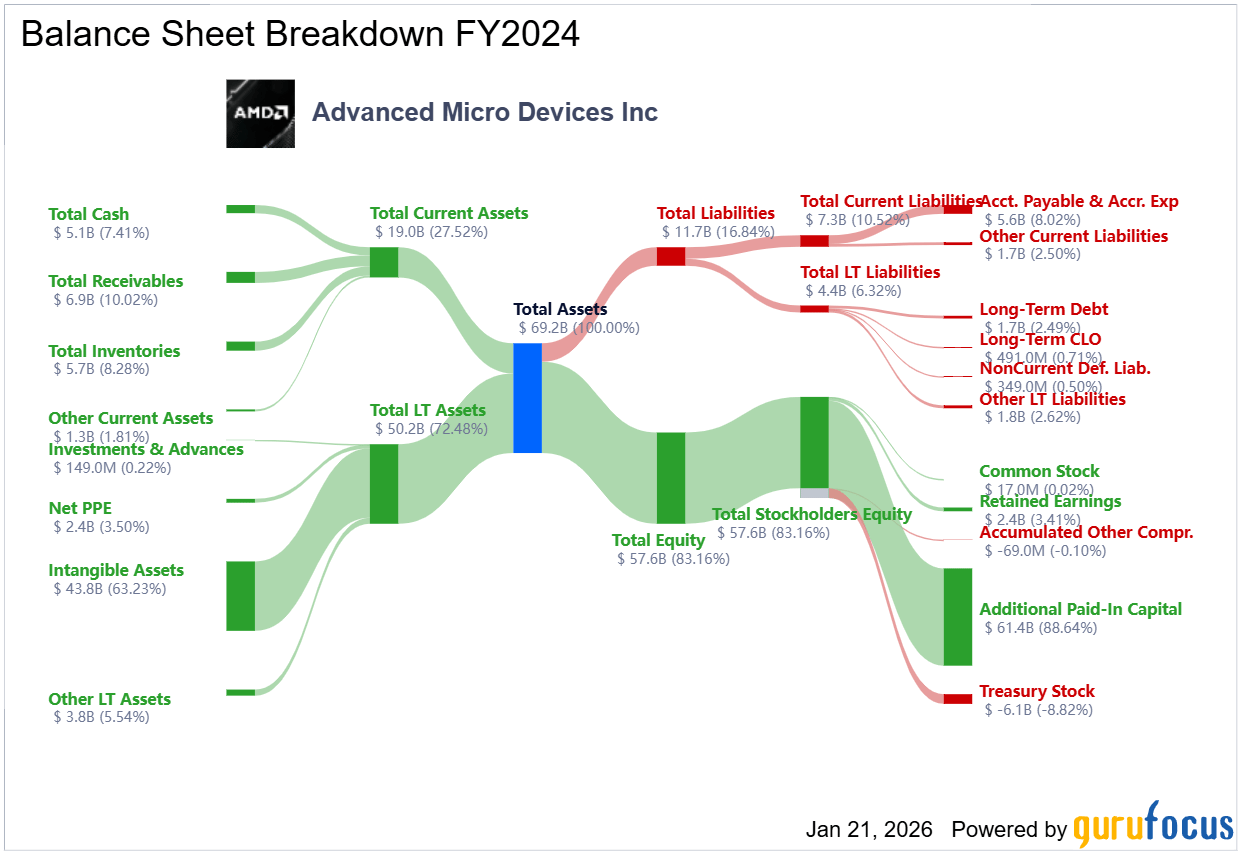

Valuation Is High, but Margins Tell the Real Story

AMD already trades at a forward earnings multiple that reflects strong optimism.

A valuation near 33 times forward earnings suggests growth expectations are baked in.

However, margin expansion remains underappreciated as a catalyst.

AMD’s gross margins trail far behind industry leaders, leaving room for improvement.

Even modest gains in profitability could significantly amplify earnings growth.

That combination of revenue expansion and margin leverage is what fuels long-term stock reratings.

Strengths

Exceptional exposure to AI and data center demand positions AMD at the center of secular growth trends.

Competitive pricing strategy increases adoption during ongoing supply constraints.

Management’s long-term visibility supports confidence in multi-year growth projections.

Weaknesses

Valuation already reflects high expectations, limiting tolerance for execution missteps.

Profitability remains well below top-tier competitors, increasing investor scrutiny.

Heavy reliance on successful AI product adoption introduces competitive risk.

Potential

Sustained 35% revenue CAGR could mathematically support a near fourfold stock increase.

Margin expansion could unlock earnings growth far beyond revenue gains alone.

Successful repositioning as a top-tier AI supplier would permanently elevate AMD’s market standing.

TODAY’S SPONSOR

AI in HR? It’s happening now.

Deel's free 2026 trends report cuts through all the hype and lays out what HR teams can really expect in 2026. You’ll learn about the shifts happening now, the skill gaps you can't ignore, and resilience strategies that aren't just buzzwords. Plus you’ll get a practical toolkit that helps you implement it all without another costly and time-consuming transformation project.

Conclusion

AMD’s growth projections are ambitious, but they are grounded in powerful industry tailwinds.

Data center acceleration combined with improving margins creates a compelling long-term setup.

For investors willing to embrace volatility, AMD offers a rare blend of scale, growth, and optionality.

Final Thought

True market leaders often emerge when perception lags reality.

The next five years may determine whether AMD becomes one of the defining AI winners of the decade.

Can I ask a small favor from you if you find the content useful to you? Spread the wealth by sharing my FREE Newsletter with fellow stock investors and friends and help to check out my sponsor advertisement and that will keep me writing more stocks newsletters!

Of course, you should always do your own research and due diligence before investing in any stock. You should also diversify your portfolio and balance your risk and reward too!

~ Final Thought: "Fortune Favors the Bold: Embrace Opportunity Property, Execute Strategy, and Reap the Rewards of Investing Wisely.”🌱

What's Your Take on Our Newsletter? 🌟We're eager to hear your thoughts so we can make our newsletter even more amazing for you! |

Disclaimer: The content provided on this blog is for educational and informational purposes only and is not intended as financial, investment, tax, or legal advice. Investing in the stock market involves risks, including the loss of principal. The views, thoughts, and opinions expressed in this blog are solely those of the author and do not reflect the views of any company, organization, or other group. Readers are encouraged to perform their own research and due diligence before making any financial decisions and actions based on the content. Neither the author nor the publisher is liable for any losses or damages arising from the use of the advice or information contained herein.

Reply