- StocksGeniusMastery

- Posts

- 💥Why Nvidia’s Pullback Could Be the Smartest AI Buy of 2026

💥Why Nvidia’s Pullback Could Be the Smartest AI Buy of 2026

The market has compressed valuation just as Nvidia prepares its next major AI chip cycle

Bensheares Parker

April 08, 2026

In partnership with

Hi Fellow Investors,

NVIDIA Corporation (NASDAQ: NVDA) has entered one of the rarest valuation setups seen in its modern market history, with forward pricing now reflecting levels usually reserved for much slower-growing businesses.

The market has become cautious, but Nvidia’s operating momentum continues to suggest that long-term demand remains exceptionally strong.

Key Points:

Nvidia’s forward valuation has compressed to levels below the broader market despite extraordinary earnings growth.

Vera Rubin may become the company’s most powerful product catalyst since Blackwell.

Current pricing creates one of the strongest long-term entry discussions investors have seen in years.

TODAY’S SPONSOR

Here’s your lifeline.

Another headline. Another client pays late. The next 10 days shift. You open your bank app before walking into the office.

The hits just keep coming right now.

And as the leader, you’re the one absorbing all of them.

But survival doesn’t come from holding tighter alone.

The Small Business Survivor Guide gives you 83 practical ways to cut costs, stabilize cash flow, and navigate economic pressure with confidence.

Because in times like these, stability isn’t luck. It’s strategy.

And the leaders who stay standing are the ones who prepare for what’s next.

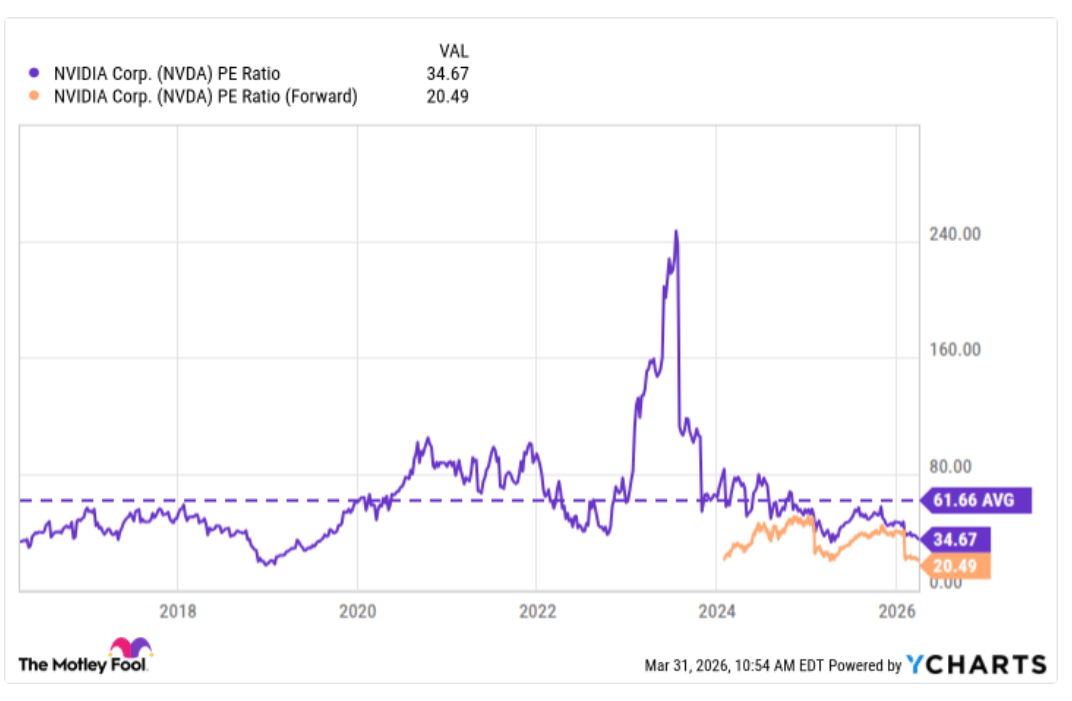

Nvidia’s Valuation Has Shifted Into Rare Territory

Nvidia’s recent pullback has pushed the stock roughly 20% below prior highs.

That decline has happened even while earnings expectations continue moving higher.

Based on projected fiscal 2027 earnings, Nvidia now trades near a forward earnings multiple around 20.5.

That places the stock below the forward valuation of the S&P 500, which is highly unusual for a company growing at Nvidia’s pace.

Historically, Nvidia has almost always traded at a significant premium to the broader market.

Why Vera Rubin Could Trigger Another Growth Leg

Nvidia’s next major catalyst is the Vera Rubin platform.

It combines Rubin GPUs, Vera CPUs, and upgraded networking systems into a more powerful AI infrastructure stack.

Management expects the platform to reduce inference token costs dramatically while improving training efficiency.

Developers may train large models using far fewer GPUs than previous generations required.

That efficiency matters because cost reduction often expands total deployment volume.

Why Customers May Accelerate Spending Even Further

Hyperscalers and frontier AI developers continue increasing compute budgets because AI workloads remain infrastructure intensive.

Lower token costs can improve margins for cloud providers while expanding usage.

That creates a powerful incentive for faster Rubin adoption.

Management has already indicated that samples are shipping and broader production begins in the second half of the year.

If deployment scales quickly, revenue acceleration could continue beyond current expectations.

Wall Street Still Expects Another Exceptional Year

Fiscal 2026 revenue reached $215.9 billion, with data center sales contributing $193.7 billion.

Consensus now expects revenue near $370 billion in fiscal 2027.

That would imply roughly 71% growth even after an already extraordinary prior year.

Adjusted earnings are projected to climb from $4.77 to $8.29 per share.

Very few megacap companies combine that earnings growth with a market-level forward multiple.

Why Some Investors View This as a Rare Long-Term Setup

Nvidia’s long-term valuation history shows that current multiples sit far below its decade average.

The stock previously traded near much richer earnings multiples when growth visibility was lower than today.

If earnings continue meeting projections, current valuation may eventually look unusually conservative.

The market’s caution largely reflects macro fears rather than deterioration in Nvidia’s business.

That disconnect is why many investors now see opportunity rather than danger.

Strengths

Nvidia still controls the most critical AI compute ecosystem across hardware, software, and networking.

Vera Rubin could create another major product cycle just as valuation has become unusually attractive.

Forward earnings growth remains exceptional relative to nearly every large-cap company.

Weaknesses

The stock still depends heavily on hyperscaler capital spending remaining elevated.

Geopolitical and macro risks can continue suppressing multiples even when fundamentals stay strong.

Expectations remain high enough that product execution must stay nearly flawless.

Potential

If Rubin adoption exceeds expectations, revenue may outpace current consensus again.

Nvidia could regain a much higher earnings multiple if macro pressure eases.

AI infrastructure demand through 2030 still implies enormous expansion potential.

TODAY’S SPONSOR

Are you tracking agent views on your docs?

AI agents already outnumber human visitors to your docs — now you can track them.

Conclusion

Nvidia rarely trades at this combination of scale, growth, and compressed forward valuation.

The market may be pricing short-term fear while long-term earnings power continues strengthening.

That is often where the strongest multi-year opportunities begin.

Final Thought

The most powerful buying windows often appear when great businesses temporarily look ordinary on valuation screens.

For Nvidia, this may be one of those unusually rare moments.

Can I ask a small favor from you if you find the content useful to you? Spread the wealth by sharing my FREE Newsletter with fellow stock investors and friends and help to check out my sponsor advertisement and that will keep me writing more stocks newsletters!

Of course, you should always do your own research and due diligence before investing in any stock. You should also diversify your portfolio and balance your risk and reward too!

~ Final Thought: "Fortune Favors the Bold: Embrace Opportunity Property, Execute Strategy, and Reap the Rewards of Investing Wisely.”🌱

What's Your Take on Our Newsletter? 🌟We're eager to hear your thoughts so we can make our newsletter even more amazing for you! |

Disclaimer: The content provided on this blog is for educational and informational purposes only and is not intended as financial, investment, tax, or legal advice. Investing in the stock market involves risks, including the loss of principal. The views, thoughts, and opinions expressed in this blog are solely those of the author and do not reflect the views of any company, organization, or other group. Readers are encouraged to perform their own research and due diligence before making any financial decisions and actions based on the content. Neither the author nor the publisher is liable for any losses or damages arising from the use of the advice or information contained herein.

Reply