- StocksGeniusMastery

- Posts

- 💥 Why ServiceNow Stock Suddenly Dropped — And What Investors Should Watch Next

💥 Why ServiceNow Stock Suddenly Dropped — And What Investors Should Watch Next

Short-term sentiment weakened, while long-term software fundamentals remain resilient.

Bensheares Parker

April 12, 2026

In partnership with

Hi Fellow Investors,

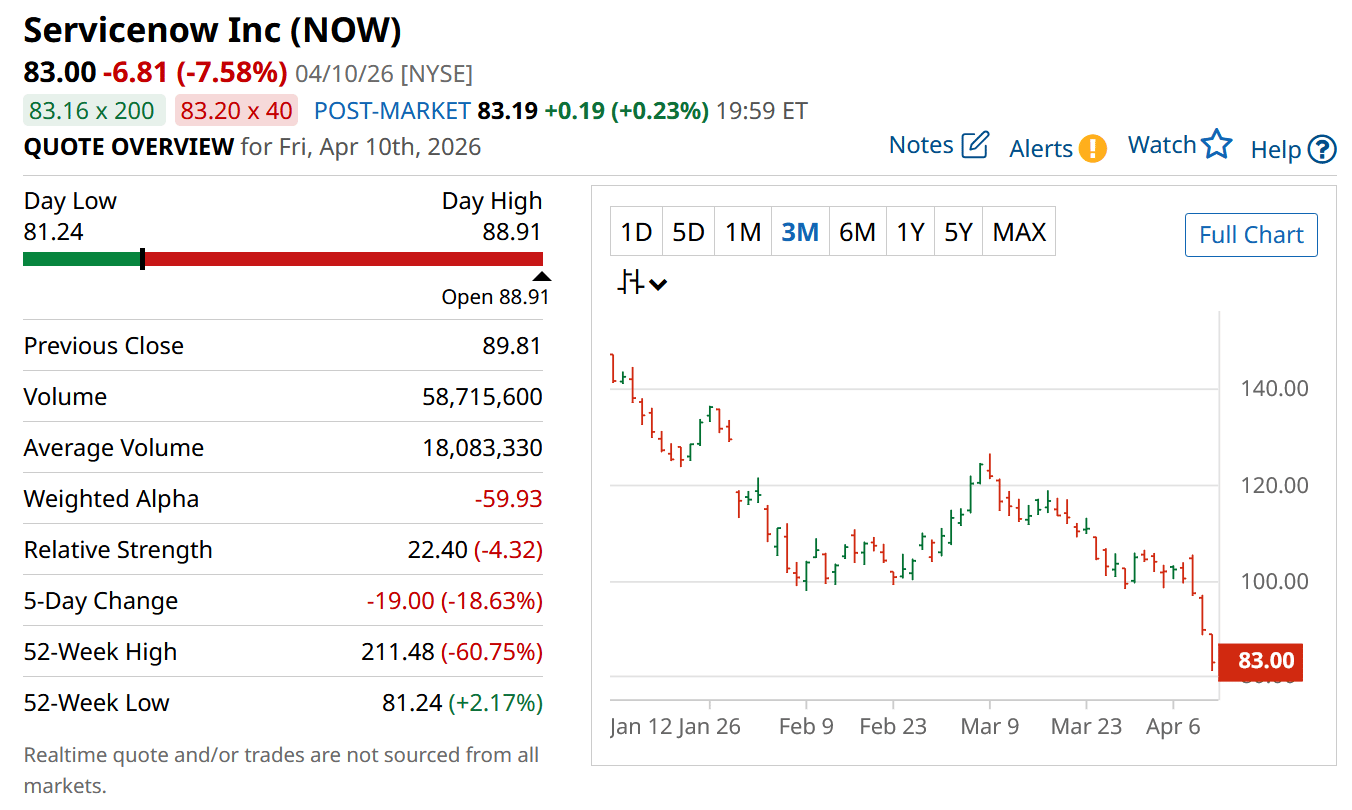

ServiceNow, Inc. (NYSE: NOW) continues to operate as one of enterprise software’s strongest workflow platforms, even though its shares are facing sudden pressure after a sharp Wall Street downgrade.

The market reaction looks dramatic, but the underlying operating targets still suggest investors should separate analyst sentiment from business execution.

Key Points:

A major price target cut from UBS triggered heavy short-term selling pressure.

ServiceNow still expects subscription revenue growth above 20% in 2026.

Expanding free cash flow margins suggest core profitability remains healthy.

TODAY’S SPONSOR

LLM traffic converts 3× better than Google search

58% of buyers now start their research in ChatGPT or Gemini, not Google. Most startups aren't showing up there yet.

The ones that are get cited by the AI tools their buyers, investors, and future hires already use. And they convert at 3×.

Download the free AEO Playbook for Startups from HubSpot and get the exact steps to start showing up. Five minutes to read.

Why ServiceNow Stock Fell So Sharply

The immediate trigger came from a sharp shift in analyst sentiment.

UBS downgraded ServiceNow from buy to neutral and reduced its price target from $170 to $100.

That kind of cut often forces short-term traders and momentum funds to react aggressively.

The downgrade reflected reduced confidence that ServiceNow will outperform peers in monetizing AI demand.

Markets often react more violently to expectation resets than to actual business deterioration.

Why UBS Became More Cautious

The core concern centers on relative AI positioning.

UBS now believes ServiceNow may not hold as clear an advantage in AI-driven enterprise software as previously assumed.

The firm also expects future quarterly results may not exceed consensus by the same margin investors had grown accustomed to.

That does not imply weakness in the core platform itself.

It simply reflects a market that now demands stronger AI differentiation from premium software names.

Why Investors Should Not Ignore the Fundamentals

Despite the downgrade, management still projects subscription revenue growth above 20% for 2026.

That remains strong for a software company of this scale.

Subscription growth continues to reflect durable demand across enterprise workflow automation.

The company also expects free cash flow margin near 36%.

That margin trajectory shows profitability is improving even as growth continues.

Cash Flow Still Makes ServiceNow Attractive

Few enterprise software businesses combine this level of recurring revenue with strong free cash generation.

Free cash flow margin has already improved steadily over recent years.

That gives ServiceNow flexibility to invest in AI features while maintaining operating discipline.

Markets often underestimate how valuable cash efficiency becomes during volatile periods.

This is one reason long-term investors often stay patient during sentiment-driven pullbacks.

Why This Pullback May Matter More for Valuation Than for Business Quality

ServiceNow had previously traded at a premium valuation because investors viewed it as a highly dependable compounder.

A downgrade naturally compresses that premium when confidence softens.

However, valuation resets can sometimes create stronger entry points if operating execution remains intact.

The key variable now becomes whether management can maintain growth while proving AI product relevance.

That will likely determine how quickly confidence returns.

Strengths

ServiceNow still holds one of the strongest recurring revenue models in enterprise SaaS.

Subscription growth above 20% remains impressive at this scale.

Free cash flow margins continue expanding, showing strong operating quality.

Weaknesses

Premium software valuations become vulnerable when analyst confidence weakens.

AI positioning is now being questioned relative to software peers.

Future earnings beats may face a higher burden of proof.

Potential

If management demonstrates stronger AI monetization, sentiment could recover quickly.

Margin expansion gives the company room to reinvest while preserving profitability.

A lower valuation may attract long-term investors seeking durable software exposure.

TODAY’S SPONSOR

Are you tracking agent views on your docs?

AI agents already outnumber human visitors to your docs — now you can track them.

Conclusion

ServiceNow’s sell-off reflects changing expectations more than collapsing fundamentals.

The company still projects strong revenue growth and improving cash generation.

For disciplined investors, execution over the next few quarters matters more than one analyst downgrade.

Final Thought

Software leaders often face sharp sentiment resets long before business fundamentals materially change.

The strongest opportunities sometimes emerge when valuation falls faster than operating reality.

Can I ask a small favor from you if you find the content useful to you? Spread the wealth by sharing my FREE Newsletter with fellow stock investors and friends and help to check out my sponsor advertisement and that will keep me writing more stocks newsletters!

Of course, you should always do your own research and due diligence before investing in any stock. You should also diversify your portfolio and balance your risk and reward too!

~ Final Thought: "Fortune Favors the Bold: Embrace Opportunity Property, Execute Strategy, and Reap the Rewards of Investing Wisely.”🌱

What's Your Take on Our Newsletter? 🌟We're eager to hear your thoughts so we can make our newsletter even more amazing for you! |

Disclaimer: The content provided on this blog is for educational and informational purposes only and is not intended as financial, investment, tax, or legal advice. Investing in the stock market involves risks, including the loss of principal. The views, thoughts, and opinions expressed in this blog are solely those of the author and do not reflect the views of any company, organization, or other group. Readers are encouraged to perform their own research and due diligence before making any financial decisions and actions based on the content. Neither the author nor the publisher is liable for any losses or damages arising from the use of the advice or information contained herein.

Reply